Dad Bought a Life Insurance for Him…

Posted on: October 17, 2016

This is, unfortunately, an all-too-common story I have heard. A new client of mine told me that his father bought a $500k variable universal life insurance policy for him 26 years ago, hoping that when he died he would leave half a million dollars to his children. (26 years ago, that was a lot of money.)

The premium for the insurance policy is $9000 a year. At some point, his dad asked him to take over the premium payments.. Between the two of them, they have already paid in a total of $234,000, but the cash value of the insurance is only $103,000.

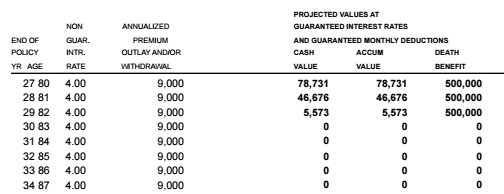

Next year, his dad will turn 80 and here is the in-force illustration the insurance company gave him. Basically, even if he continues paying the premium, his insurance will lapse when his dad turns 83, a mere four years from now. If that happens, they will have paid $270,000 to the insurance company, all for nothing. To avoid that outcome, his dad literally has to die in within the next four years.

When his dad turns 80, the mortality expense of the life insurance escalates to $40k – $50k per year, far more than the annual premium. The shortfall has to be drawn from the cash value. That’s why the cash value will dwindle fast. When there is no cash value left, the insurance lapses.

My client is left with the unenviable options of either:

- Surrendering the insurance and taking out the cash value, which means accepting $103k of loss without the benefit of a tax write off.

- Keep paying the premium and hoping his dad won’t live past 83.

If you truly want to leave something to your children other than financial loss and headache, try true investment, like a 50/50 portfolio in stock and bond index funds. If my client’s dad had done that, putting $9000 into such a portfolio every year, he would have left his son with $670k.

Schedule a Discovery review with me, or get my white paper for free: The Informed Investor: 5 Key Concepts for Financial Success.

October 18, 2016 at 9:54 am

The premiums are a sunk cost. They’re gone, with no way to recover them and no point in worrying about them. If it were me in this situation, then I would wait until parent is 79+11 months and take the maximum cash value. (It is easier to be objective when you’re not involved.)

My parents did something almost as bad. They took out a whole life policy on me soon after I was born. They were convinced by the salesman that it was an investment. It was, but a bad one. I did get a few thousand dollars out of it when I was in my early 20s, learning in the process what a bad deal insurance is as an investment. So I guess I did get more out of it. I’ve never “invested” in any insurance. I use term policies as pure insurance, and invest in low cost index funds.