Archive for the ‘Life’ Category

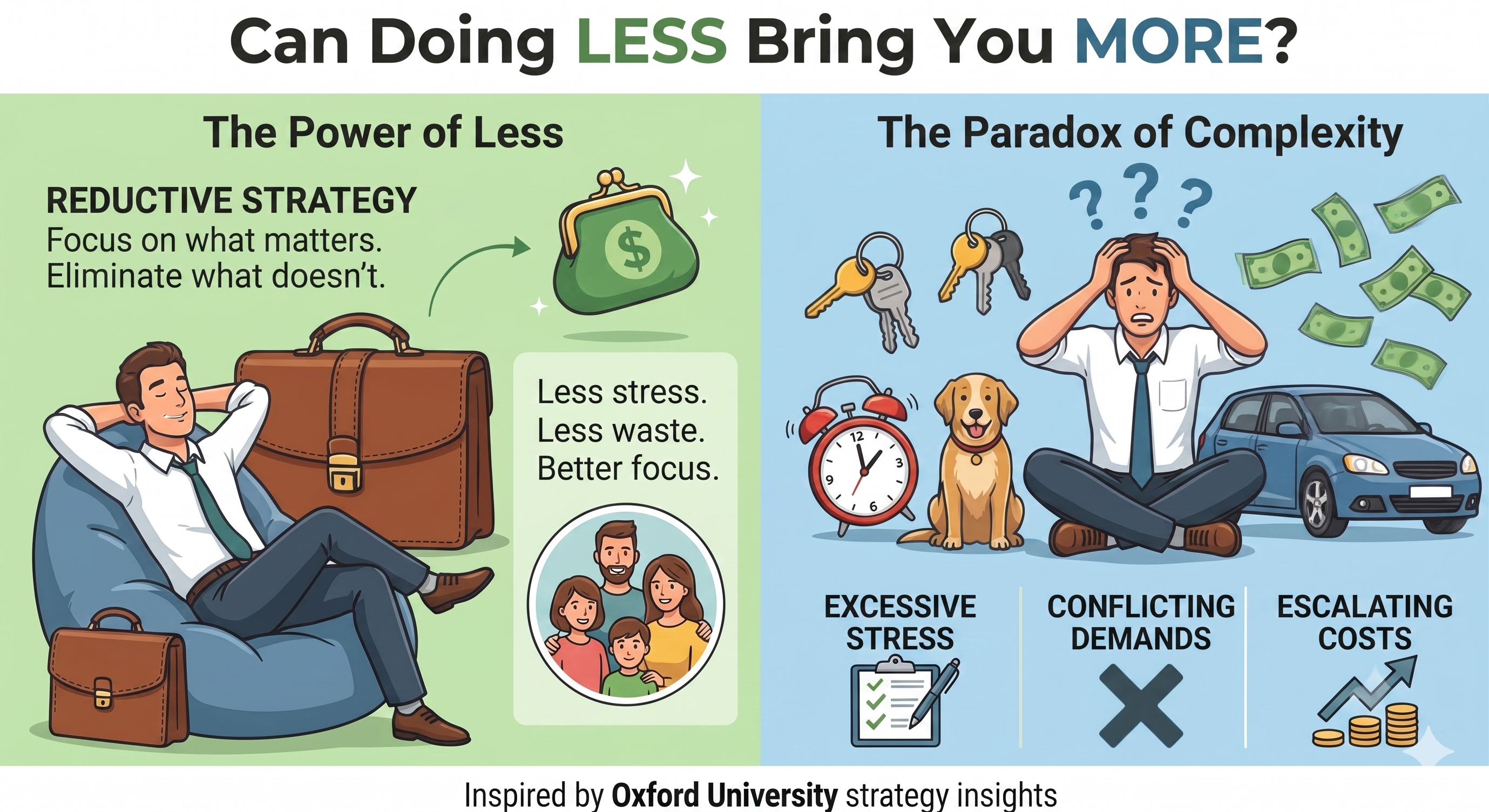

During the Oxford Reunion Week, I had many interesting conversations with classmates who were attending the strategy class. I took the same class five years ago, and today I would like to share my biggest takeaway from it – reductive strategy.

What is Reductive Strategy?

When it comes to strategy, most businesses ask, “What more can we do?” Professor Whittington suggested that we ask a different question instead: ”What else can we stop doing?” This question forms the foundation of reductive strategy.

Take my own line of business for example. Most financial advisory firms try to be all things to all people. Some firms even offer to walk clients’ dogs and to be their golf partners. They believe this makes them more competitive. Drawing from the insight of reductive strategy, I don’t do any of those that is 1) not my core competency, 2) not what my clients come to me for. This strategy has helped me build a simple but elegant practice.

Great Savings from Reductive Strategy

Read the rest of this entry »Share this:

Recently, I’ve noticed a recurring theme in my conversations with clients and friends: economic anxiety, even among those who are financially well-off.

Take, for example, a friend of mine who works at Meta. With total compensation exceeding $350,000, she’s comfortably in the top tier of American income earners. Yet a large house, a luxury car, and costly extracurriculars for her children mean she’s living paycheck to paycheck.

On top of that, her work demands are immense. Not only does she work standard office hours, but late-night meetings with overseas suppliers are a daily occurrence, leaving her burnt out and longing for a less demanding role. However, the thought of a pay cut and the lifestyle changes it would bring prevent her from exploring alternatives, even as her health suffers.

She recently came to me for a second opinion financial review. While I didn’t magically solve her issues overnight, I did provide clear direction. The relief she experienced was so tangible that she shared her experience with several Meta colleagues, all of whom reached out for similar guidance.

Read the rest of this entry »Share this:

- In: Life

- Leave a Comment

The eBook version of my book “Entrepreneur Wealth Management Made Easy” is now free! on Amazon for the next three days. Go get it: https://shorturl.at/xKa8z

Note that Amazon will try to lure you into subscribing to their KindleUnlimitedwith the first big yellow button “Read for Free”, avoid that. Click the second deeper yellow button “Buy now with 1-click” instead.

This is my New Year gift for all entrepreneurs out there. Please forward to your entrepreneur friends.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

- In: Life

- Leave a Comment

Thank you so much to everyone who responded to my recent request for your opinions. Let me cut to the chase: 45% of you want me to write about the latest academic research; 36% want to hear about cautionary tales, and 19% want both – one person even suggested that I should be able to combine the insights from academic research with cautionary tales.

Cautionary tales are relatively easy to write since they are direct results of f my work with my clients. I often deal with things they did before I started working with them or things I wish they had discussed with me before acting.

It is much more challenging to write about academic research. Most academic papers are very abstract and they are scattered throughout various journals. I must first survey these journals and extract useful insights from them.

If writing a cautionary tale is an 1-hour job, writing about academic research could take 10 hours. But I will do that since that’s what you have asked me to do. And, quite frankly, writing about these studies will help me better manage my clients’ wealth.

Here are the journals that I will survey:

Read the rest of this entry »Share this:

I was invited to a dinner by a client couple of mine. Their youngest daughter has been accepted to three universities and they are having a hard time picking the right one and they wanted my help.

Universities A and B are both out-of-state Ivy League universities that cost more than $60k a year in tuition. University C is an in-state university that costs only $15k. I listened to their reasoning as to why it is so hard to make a decision. They really want to give the best to their daughter and besides, an Ivy League university would give them a lot of face (there you know they are a Chinese American family) since their peer families all brag about their children’s academic achievements and they feel pressured to keep up.

Before I said anything, I forewarned them that the choice of university is a very personal one for them and their child so they should take my words only as my observations and not as my professional advice.

First, since universities A and B are four times as expensive as university C, do they provide four times more value? By this I mean, would their child acquire four times as much knowledge or earn four times as much after graduation? (I will get to this point later.) If not, they would be paying the extra just for the bragging rights.

Second, what financial values do they want to impart on their children? That they should borrow money to pay for something they can’t afford just for vanity? Would such a value system not lead to financial ruin for their children down the road?

Read the rest of this entry »Share this:

Today I had a very productive meeting with a long-time client of mine. At the end of the meeting, I mentioned that he appeared to have lost quite a bit of weight and he went on to tell me that through diet, exercise and some medications, he was able to reverse his diabetes. I am so happy for him! He is truly making the best investment in his life!

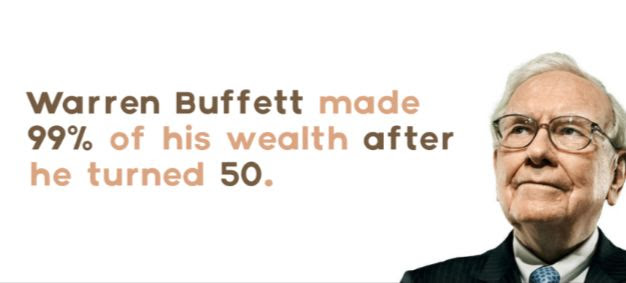

Did you know that Warren Buffet made 99% of his $90b wealth after he turned 50? To be more exact, he did it after he turned 54. Now he is 91. So how did he do that? After all, he is such a boring investor! He missed the best moment to get into AAPL. To this day, he is still not invested in TSLA and he totally doesn’t understand Bitcoin. In his entire investment career, he has rarely had a blockbuster win. So how on earth did he accumulate so much wealth? One often-overlooked reason is that he has lived a very long life.

Share this:

My 2021 Highlights …

Posted on: December 30, 2021

- In: Life

- Leave a Comment

I had a blessed 2021! Here are the highlights.

1) Finished all my Oxford courses.

2) Produced a Showstopper improvised musical show for my Oxford classmates at Oxford.

3) Visited the Balkans, especially “the Bridge over Drina.” Learned about its fascinating and tortured history.

4) Took my kids to many Western European cities/towns.

5) Continued my hip hop adventure with Doug. Now I can more or less rap freestyle!

6) Started learning German. With help of a fantastic teacher Kat, I can now speak broken German.

Read the rest of this entry »Share this:

Funny Tidbits at Oxford

Posted on: October 14, 2021

- In: Life

- Leave a Comment

Last Saturday I completed my executive MBA study at Oxford. The whole thing actually started quite serendipitously. A client of mine who is a physician studied there and he liked it so much that he encouraged me to apply. Today I’d like to share some funny moments on my journey.

As part of the application process, I went to Oxford for an interview. I booked a student dorm room at Sommerville college, and when I checked in, I was mesmerized. The dorm room looked and smelled like it was right out of a Harry Potter movie. The adjacent canteen looked like the Great Hall at Hogwarts, with walls adorned with huge classical paintings of accomplished women alumni.

That night I was the only resident in the entire building, and it didn’t take long for me to notice that the bathrooms were not marked by sex, and in fact there were no male bathrooms. Later I found out that Sommerville is the first girls’ college at Oxford and Margaret Thatcher herself graduated from there.

Read the rest of this entry »Share this:

- In: Life

- Leave a Comment

I admit this is not exactly an investment piece. However, if you continue to read, it might yet turn out to be your best investment. Study after study has shown that what determines life satisfaction is not money, but relationships you are able to build with other human beings. Come to think of it, our lives are but tapestries of woven human connections. The stronger the connections, the happier and resilient you are. And what better way to strengthen your most important relationships than gifting meaningful songs during this holiday season. You can get a song custom-made for your loved ones on this website: http://VeryOwnSong.com.

Read the rest of this entry »Share this:

Can Doctors Die Poor?

Posted on: October 20, 2020

This is the opening story of my book “Physician Wealth Management Made Easy” published nearly three years ago. It was briefly the Amazon Bestseller in the physician category.

Twelve years ago, I got a call from my internist. “Michael, I am afraid I can’t be your doctor any more,” he said, right after hello. It was an odd opening, and his voice sounded strained. Doc Johnson and I had always been on friendly terms. Had I done something wrong to offend him?

“What’s going on, Doc?” I replied. “Is it .. is it my insurance?”

“No, Michael,” he said and took a deep breath. “I’ve been diagnosed with pancreatic cancer. And …” he paused again. “I have only a few months to live.”“Wow, that’s terrible, Doc.” I didn’t quite know how to go on and ask, “OK, but why did you call me? I am no doctor. What can I do about it?” So I just waited on the line.

Read the rest of this entry »Share this:

- In: Life

- Leave a Comment

1, I got accepted into Oxford University Business School’s Executive MBA program. I will go to Oxford to attend classes starting in January. The program requires me to go to Oxford one week out of every five for a year and a half with a total of sixteen modules.

2, I’ve nearly finished my second book “Entrepreneur Wealth Management Made Easy.” I expect to publish it in the first half of the new year.

Share this:

I Am In The News For This …

Posted on: January 16, 2018

- In: Life

- Leave a Comment

DC Metro Theater Arts, the largest performing arts publication in the Mid Atlantic region, just did an article about the upcoming improvised musical show I am producing in Bethesda. Tara and Rance, the two performers from Chicago, deservingly got the lion share of coverage, but the publication did say this about me:

Their upcoming show at Imagination Stage in Bethesda will be their first in that venue and in Maryland. This opportunity landed on their radar through Michael Zhuang, a resident of Bethesda, nicknamed “The Investment Scientist” for his founding of MZ Capital Management. Mr. Zhuang has traveled the world and spent countless hours researching, studying, and practicing his love of musical improv. In 2017, he began sponsoring up-and-coming talent from the improv-comedy meccas of New York City and Chicago to perform locally, with the goal to embed musical improv into the fabric of Bethesda’s growing arts and entertainment culture.

“My vision is to see Bethesda’s performing arts scene flourish,” said Zhuang.

Share this:

Happy 2018! Unforgettable 2017!

Posted on: January 2, 2018

- In: Life

- Leave a Comment

-

I published my first book “Physician Wealth Management Made Easy” and it got off to a strong start. It was Amazon’s #1 Hot Release in the Physician category for a month.

-

I auditioned and was accepted into the cast of the DC production of the Broadway musical, Chess. I even got to sing five lines of solo in the opening scene, “The Story of Chess.”

-

My business grew 33%. Now $100mm AUM is within reach. I was also recognized as one of Top 100 Influential Advisers by Investopedia on strength of my knowledge

contribution.

-

I performed an improvised musical format called Spontaneous Broadway at San Francisco’s Bayfront Theater. I also performed an improvised musical solo at the Source Theater in DC.

Share this:

I Did a Terrifying Thing …

Posted on: August 1, 2017

- In: Life

- Leave a Comment

Spontaneous Broadway is an hour and a half long musical show broken into two 45-minute sections. In the first half, the audience members are asked to write down made-up song titles and put them a basket. Each actor in the cast will draw one from the basket and, based only on the title, make up a song right on the spot. Afterward, the audience will vote for the song they like the best.

In the second half of the show, the cast will create a Broadway musical that contains the song the audience picked along with many other songs, characters and a story. This, again, is done entirely by improvisation.

Just the thought of this terrifies me. That’s why I flew to San Francisco last week to participate in a workshop put on by Bats Improv Theater. The conclusion of the workshop was a public performance this past Sunday.

Oh boy! Did we (the student cast) did an awesome show?

Share this:

I am among Investopedia 100

Posted on: July 15, 2017

- In: Life

- Leave a Comment

Well, two weeks ago I got an email from Investopedia, an encyclopedia website for personal finance and investment. The email told me that I was recognized as one of their “Top 100 Influential Advisors” in their inaugural ranking.

Let me just say I was very skeptical. I’ve gotten emails like that before, sometimes even from reputable magazines, telling me that I had been selected in their top financial advisor rankings. They then would go on to ask me to buy advertising, or make a payment to retain my listing in their top advisor rankings.

Share this:

Beware of Financial Advisor Awards

Posted on: May 3, 2017

- In: Life

- Leave a Comment

Am I super excited about this recognition?

Hardly!

This is not the first time I’ve gotten this type of email. In the past, I have received similar emails from both strangers and people claiming to represent well-recognized publications like Barron’s and Forbes. They all told me that they wanted to recognize me as the best wealth manager/financial advisor/financial planner in the country, or in my state, or in my city, or ever born. Read the rest of this entry »