Archive for the ‘Security Selection & Market Timing’ Category

A client of mine recently asked me a great question: “What value did you bring to our engagement?” To answer this, we went back to look at the net profit of his account since 2019.

2019: $151k

2020: $197k

2021: $286k

2022: -$323k

2023: $304k

2024: $232k

2025: $311k

2026YTD: $129k

Then he asked an even better question: “That doesn’t mean you added substantial value, does it? If I had just invested the money in the S&P 500, I could have made the same amount or even more.”

So I further clarified …

Read the rest of this entry »Share this:

Continuing the streak of writing about the most prominent academic research papers on finance and investment, today I will write about “Returns to Buying Winners and Selling Losers,” which was published in 1993 in the Journal of Finance and is currently the third most highly quoted paper in history.

The authors, Narasimham Jegadeesh and Sheridan Titman, studied whether there is persistent money to be made by buying winners and selling losers, otherwise known as the momentum strategy. If the answer is yes, what is the best way to execute it?

They found that if one buys a portfolio of winners (stocks with the top decile returns in the previous 12 months) and sells a portfolio of losers (stocks with the bottom decile returns in the previous 12 months), and holds that for 3 months, one can achieve a return of 1.49% per month on paper. This is huge! This level of monthly returns translates into nearly 18% annual return.

Throughout my 20 years of giving financial advice, I have noticed that amateur investors love momentum strategy, while more mature investors shun it because they have learned the caveats.

So what are the caveats?

Read the rest of this entry »Share this:

This is an article I wrote fourteen years ago that was inspired by Daniel Kahneman’s Nobel Lecture “Maps of Bounded Rationality.” Here I will repost it without changing one word – I am proud of the evergreen nature of my articles. At the end, I will make a few additional comments in red that include new insights from the last fourteen years.

Do you know that the top three one-day drops in Dow Jones happened in October? On the 19th of October 1987, Dow Jones fell nearly 23%, making the day the worst day in the US stock market history. It was followed by the 24th and 29th of October 1929, when Dow Jones fell 13.5% and 11.5% respectively, ushering in the Great Depression. These events are commonly remembered as the crash of 29 and the crash of 87.

Read the rest of this entry »Share this:

In June of 2007, I wrote my first article on stock market seasonality. There I wrote that there was a rather persistent and robust stock market phenomenon that the market tended to perform well in the winter months than in the summer month. By “persistent” I meant that it lasted for decades in the US market, by “robust” I meant that the phenomenon showed up in other stock markets as well, as can be seen by this chart.

Share this:

A few days ago, I was approached by an employee of Nvidia regarding his $5mm worth of NVDA stock. A Morgan Stanley broker had pitched him the idea of using exchange funds to diversify his holdings and he wanted my second opinion.

A few days ago, I was approached by an employee of Nvidia regarding his $5mm worth of NVDA stock. A Morgan Stanley broker had pitched him the idea of using exchange funds to diversify his holdings and he wanted my second opinion.

If you are an employee of any of those high flying tech companies like Amazon, Facebook, Google, Apple, Microsoft, Netflix, and etc., you are likely to have been pitched such an idea. Talk to me before you execute anything.

So what exactly are exchange funds? Exchange funds are unregistered private-placement limited partnerships or LLCs designed specially for investors with concentrated positions in highly appreciated stocks to help them diversify without triggering taxes.

How do they work? Investors transfer shares of their concentrated stocks to the fund in exchange for an equal value of units of the fund. These transfers are not taxable since they are considered partnership capital contributions under the tax law. There are a few caveats to the law though: investors have to stay in the fund for a minimum of seven years and the fund must invest 20% of its capital in illiquid assets.

Share this:

I asked my assistant to do an updated stock market seasonality study.

The data we used was the S&P 500 index from 1927 which we found in Nobel Prize winner Robert Shiller’s database.

We assumed that at the beginning of each year we invested $1 in the index, and we observed how the investment fluctuated over the year. Then we took the average over three different periods of time: the last 20 years, the last 50 years, and the last 86 years.

Here is the chart we got: Read the rest of this entry »

Share this:

Are There Rebalance Bonuses?

Posted on: February 24, 2014

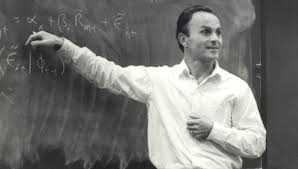

Professor Kenneth French

Last month I did a study to understand why equally weighted the S&P 500 index RSP has outperformed value weighted S&P 500 index SPY by almost 3% a year since its inception. My conclusion is that it’s mostly due to Fama French risk factor loading.

However, my research also found after removing the effect of risk factors, RSP has a slight alpha advantage over SPY. I conjecture this alpha advantage is due to the fact that RSP requires annual rebalancing and SPY does not. In other word, this could be the so-called “rebalance bonus.”

To test its robustness, I extended my study to six pair of Fama French “indices.”

Share this:

According to Nobel Laureate Eugene Fama, there are three major risk premiums.

According to Nobel Laureate Eugene Fama, there are three major risk premiums.

1. Equity premium is the additional “wage” one can earn from taking stock market risk over not taking stock market risk.

2. Small cap premium is the additional “wage” one can earn from taking small company risk over taking large company risk.

3. Value premium is the additional “wage” one can earn from taking non-growing company risk over taking growing company risk.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

Since its inception on March 9, 2003, RSP has returned 193%. At the same time, SPY has only returned 97%. This is extremely puzzling as both RSP and SPY hold the same S&P 500 stocks.The only difference is that SPY is a cap-weighted fund and RSP is an equally-weighted one. This begs the question, is RSP’s outperformance normal; and more importantly, is it likely to continue?

Since its inception on March 9, 2003, RSP has returned 193%. At the same time, SPY has only returned 97%. This is extremely puzzling as both RSP and SPY hold the same S&P 500 stocks.The only difference is that SPY is a cap-weighted fund and RSP is an equally-weighted one. This begs the question, is RSP’s outperformance normal; and more importantly, is it likely to continue?

To answer the question I asked my intern Nahae Kim to run a regression based on the Nobel Prize winning Fama-French Three Factor Model.

R(x) – rf = alpha + beta1*(Rmkt – rf) + beta2*SML + beta3*HML

Where R(x) is the return of the selected fund, x being either RSP or SPY, alpha is the “skill” of the fund, beta1 is the market risk loading, beta2 is the small cap risk loading and beta3 is the value risk loading.

Here is what I got from the two regressions.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

It is exceedingly difficult for mutual funds to beat market indexes. For the past decade, Standard and Poor’s has methodologically documented returns by mutual funds and what they found is something those fund managers do not want you to know: the majority of mutual funds under-performed their respective indexes literally every single time.

It is exceedingly difficult for mutual funds to beat market indexes. For the past decade, Standard and Poor’s has methodologically documented returns by mutual funds and what they found is something those fund managers do not want you to know: the majority of mutual funds under-performed their respective indexes literally every single time.

Here is an infographic published by MoneySense, a Canadian financial magazine, that shows 90% of Canadian money managers under-performed the market index in 2012; I can assure you that US money managers are doing no better.

Share this:

Recently a business owner asked me to review his investment portfolio. He is currently with an Ameriprise financial advisor and his gut feeling tells him something is amiss.

Recently a business owner asked me to review his investment portfolio. He is currently with an Ameriprise financial advisor and his gut feeling tells him something is amiss.

He is paying the advisor 1.6% in fees. First of all, this fee is quite exorbitant. For the size of his portfolio, he shouldn’t be paying more than 1% in advisor fees.

Adding insult to injury, for the fee that he is charging, this advisor puts his money into a collection of very expensive mutual funds like ODMAX.

It is very easy to check the expenses of a mutual fund. I just googled ODMAX and I found out it has a load of 5.75% and an expense ratio of 1.36%. (For those who don’t know, load is a one time charge to pay commision to the Ameriprise advisor who doubles as a broker. Expense ratio is an ongoing annual charge.)

ODMAX is a mutual fund that invests in emerging market stocks. If you use the low cost alternative, aka a Vanguard fund, you will pay no load and the expense ratio is only 0.33%, a saving of 1.06%.

Don’t ever underestimate these tiny savings. Because in ten years, the savings will be more than 10%, in twenty years, more than 20%. This businessman is in his 50s; he can easily live another 30 years. I asked him: “How would you like to be more than 30% poorer in retirement?” That is exactly what this financial advisor will make him.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

As far as investment philosophy is concerned, I am solidly in the camp of Nobel Prize winner Eugene Fama and Vanguard founder Jack Bogle. They both believe that the market is by and large efficient, and there is no point in picking stocks.

As far as investment philosophy is concerned, I am solidly in the camp of Nobel Prize winner Eugene Fama and Vanguard founder Jack Bogle. They both believe that the market is by and large efficient, and there is no point in picking stocks.

Most of my money is in broad-based passively managed asset class funds, but I do set aside 5% just to have some fun with and right now I only have three stocks in my fun account.

Safeway

I bought SWY last November after going to the Chicago Booth Entrepreneur Advisory Meeting. From the meeting, I learned that big retailers routinely write off their inventory at a huge loss. The reason being that they can not control demands as they have little information about the needs of the individual consumer, though they can usually make a rough guess on aggregate needs.

I noticed my wife had been shopping at Safeway more and more. After a little digging, I found out Safeway had set up a technology system to track each individual’s needs and price sensitivities. Then it can make targeted offers to shoppers like my wife that unfailingly brought her back over and over. I recalled my earlier meeting and realized they would save tons of money just from better inventory management.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

It really caught me by surprise when Eugene Fama, the newly minted Nobel laureate in Economics said: “It doesn’t matter that much.” when speaking about investing outside of the US.

It really caught me by surprise when Eugene Fama, the newly minted Nobel laureate in Economics said: “It doesn’t matter that much.” when speaking about investing outside of the US.

OK sure, I can understand his point. Why invest outside of the US when the US markets already account of 40% of world capitalization? “The U.S. market is so well-diversified already that combining it with global markets doesn’t really matter,” so said Fama.

However, I think it actually does matter ….

Proportionally, the US market is getting smaller. Right after the second world war, the US market accounted for 70% of world capitalization, now it only accounts for 40%. For a country that boasts only 5% of of the world’s population, this is still exceptionally high.

For the foreseeable future, there are better than even odds that the combined markets outside of the US will grow faster than the US market will do alone. Why forego those opportunities?

The diversification benefit you’d get is certainly not negligible either. During the so-called ‘lost decade’ of 2000 to 2009, the US market, as measured by the S&P 500, had a net loss of 9.1%, while international developed markets went up by an anemic 12.4%, but emerging markets went up by a whopping 154.3%.

It would have made a bog difference if you have a piece of emerging markets in your portfolio.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Request White Paper | Request Discovery Meeting

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

I jumped out of my chair in delight when I learned that Eugene Fama and Robert Shiller had won this year’s Nobel Prize in Economics. These are two economists that greatly influenced my investment philosophy and their works have been an integral part of how I help my clients build and preserve wealth.

Let me explain their contributions:

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

10. P2P Lending: A New Asset Class?

10. P2P Lending: A New Asset Class?

9. A Lesson From a Client: Celebrity Business Gone Bad

8. The High Cost of Fee-Based Financial Advisors

7. How Often Do Market Corrections Happen?

6. Captive Insurance: A Business Owner’s Heaven?

5. How I Helped a Client Save $100k in One Meeting

4. Variable Annuity Fees You Don’t Know You are Paying

2. Be Careful When Buying a Condo as a Rental Property

1. Profit from Harry Dent’s Prediction? Think Again

Also see Top Ten in July.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Request White Paper | Request Discovery Meeting

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

1. ThinkAdvisor highlighted a Maryland study which showed that states which pay the highest fees to Wall Street (for managing pensions) have the lowest returns. That says it all about Wall Street. No wonder Rick Ferri wants you to steer clear of actively managed funds.

1. ThinkAdvisor highlighted a Maryland study which showed that states which pay the highest fees to Wall Street (for managing pensions) have the lowest returns. That says it all about Wall Street. No wonder Rick Ferri wants you to steer clear of actively managed funds.

2. Reuters Money reported how Health Savings Accounts (HSAs) can be used as retirement savings accounts. This information is especially useful for small business owners and self-employed individuals who tend to neglect their retirement savings and face high deductibility in their health insurance. Here is the garden variety of ways they can save for retirement.

3. DIY Investor Robert Wasilewski encountered a bear while hiking. He survived to write about it, but he mused that the same reactions that kept him in the gene pool will surely “eliminate you from the investment pool.”

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter