Archive for the ‘Conflict of Interest’ Category

If your Financial Advisor has Conflicts of Interest: Three Quick Ways to Determine

Posted on: September 6, 2024

In my last newsletter, I wrote about finding $50k+ worth of hidden costs due to conflicts of interest, and a reader asked me if there is a quick way to check if her financial advisor has such conflicts. Her question inspired my article today.

Before we dive into that, I must first give you a quick overview of the legal environment in which financial advisors operate. There is the Securities Exchange Act that regulates brokers and does NOT require them to act in the best interest of their clients, and there is the Investment Adviser Act that regulates RIAs (registered investment advisors) which does require them to act in the best interest of their clients.

Your financial advisor can be a broker, an RIA, or even dually registered. Those dually-registered ones can be especially deceptive. Here is an actual example – the last few lines of a financial advisory firm’s website:

Read the rest of this entry »Share this:

This morning, I did a portfolio review for a 2nd Opinion Review customer. It is a portfolio worth just under $4mm and I found $56k of hidden costs per year.

Load is the least hidden of all hidden costs, it is a one-time charge that happens when the broker (“financial advisor”) puts your money in a mutual fund. The mutual fund immediately takes a percentage of your money and gives it to the broker as commission. Since this is too obvious, few brokers are that blatant these days.

Expense ratio is the percentage the fund deducts from your investment, and part of this deduction is given to the broker as a kickback. It is even more costly since it occurs every year. It creates an adverse incentive, since the broker is more inclined to put your money in funds that give them a higher kickback. The gold standard of expense ratio is 0.05%. Note that many funds in this analysis have an expense ratio over 1%, over twenty times more expensive than the gold standard.

Turnover measures how frequently the fund manager churns your investments. The more frequent the churn, the more money you lose and the more money the brokerage that handles the trades makes. The gold standard of turnover is less than 10%. If a fund has more than 100% turnover, it belongs in the category of horrible, since 100% equates about 1.2% loss of return.

See below the result of the portfolio review. Numbers in yellow are bad, numbers in red are outright horrible. Compare these numbers to the numbers in green, which is our gold standard.

Read the rest of this entry »Share this:

I have done many portfolio reviews over the years and I’ve seen all kinds of mistakes people make with their investments. Starting today I will do a series of articles on this specific topic. Hopefully, you will learn from these examples and therefore avoid repeating them.

First let me clarify a couple of terms:

- Financial Advisor: the guy who gives you financial advice and tells you where (what funds) to invest your money. Most of them work for big brokerages like Merrill Lynch, Morgan Stanley, and others (therefore the conflict of interest), and most of them can direct your money.

- Fund Manager: the guy who works at a mutual fund who does not interact directly with you, but nevertheless decides what stocks and bonds or other funds your money should be invested in once your financial advisor has invested your money in his fund.

To review a portfolio, first and foremost, I examine the hidden costs:

Read the rest of this entry »Share this:

Today I finally finished the Oxford class on Private Equity, and I’d like to share with you, my readers, some of my takeaways.

Long-time readers of my newsletter should know that I have long advised against investing in private investments unless 1) you know the business and 2) you have a measure of control. The reason for this is that private investments are not under the purview of the SEC, and thus provide a fertile ground for conflict of interest. After the Oxford course on private equity, I feel completely vindicated.

Some of my readers, if you are wealthy enough, will be approached with private equity investment opportunities. You will be presented with mouth-watering return numbers. My professor called these numbers complete “garbage,” they can be manufactured (but not fabricated.) Fabricating numbers is against the law, but manufacturing numbers is not, and there is only a hair’s breadth separating them. Next time you see a number like 36.8% annual return, think “manufacturing” and don’t waste your time! I will show you how they manufacture numbers in the next article.

Read the rest of this entry »Share this:

Part of Wall Street analysts’ job is to make earning forecasts of covered firms so as to guide investors’ actions. In 1996, Professor Rafael La Porta discovered an interesting phenomenon: the better the forecasts, the worse the returns! Twenty years have passed since his last paper, now we have two more decades of data. Does the new data confirm or contradict his original discovery? Well, see this graph, which I lifted right from his new paper.

Share this:

Unexpected Horrible Tax on IRAs

Posted on: October 21, 2019

How would you feel if you were told by your broker that your IRA had to pay $60k in taxes to the IRS? This is not just some grim fairytale, this is actually happening to a new client of mine. I share this horror story so all of you can learn something.

The IRA account was transferred under my management last year. The entire amount was invested in a private partnership, something I have never thought highly of. They are an investment vehicle that is unregulated and not registered with the SEC and thus is not supposed to be sold to the public. They nevertheless find their way into wealthy investors’ portfolios since brokers love to peddle them due to their exorbitant fees. My client invested in 2006, long before he became my client. After 13 years, it has a grand total return of only 40%. A 50/50 portfolio of stock and bond index fund would have more than doubled his money over the same period of time.

Share this:

I’ve done a lot of second opinion financial reviews over the years and these fees are broadly consistent with what I’ve seen in portfolios managed by Wall Street brokerages like Merrill Lynch, Morgan Stanley, Ameriprise etc.

In comparison, my fees are 1% for the first million, 0.7% for amounts up to $5mm and 0.4% for amounts over $5mm. Most independent RIAs (registered investment advisers) are like me – our fees are about a third of those by major brokerages.

Everything else being equal, if you are paying 1.5% more a year in fees, a back-of-the-envelope calculation will tell you that in 20 years you will be 30% poorer because of those higher fees. In 30 years, you will be 45% poorer.

But everything else is not equal. There are two other major distinctions between brokers and RIAs: Read the rest of this entry »

Share this:

This is, unfortunately, an all-too-common story I have heard. A new client of mine told me that his father bought a $500k variable universal life insurance policy for him 26 years ago, hoping that when he died he would leave half a million dollars to his children. (26 years ago, that was a lot of money.)

The premium for the insurance policy is $9000 a year. At some point, his dad asked him to take over the premium payments.. Between the two of them, they have already paid in a total of $234,000, but the cash value of the insurance is only $103,000.

Next year, his dad will turn 80 and here is the in-force illustration the insurance company gave him. Basically, even if he continues paying the premium, his insurance will lapse when his dad turns 83, a mere four years from now. If that happens, they will have paid $270,000 to the insurance company, all for nothing. To avoid that outcome, his dad literally has to die in within the next four years.

When his dad turns 80, the mortality expense of the life insurance escalates to $40k – $50k per year, far more than the annual premium. The shortfall has to be drawn from the cash value. That’s why the cash value will dwindle fast. When there is no cash value left, Read the rest of this entry »

Share this:

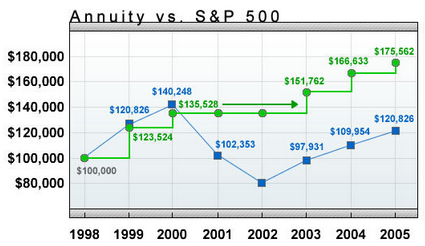

Typical Salesman’s Chart for EIA

Financial author Allan Roth once wrote an article called “Investment Trick – Annuity Style” where he asks a rhetorical question, “If the S&P 500’s total return is 12% in a given year, what do you think your equity index annuity (that is supposed to track the S&P 500) would return”?

- 10%

- 8%

- 5.4%

- 3.4%

Allan Roth goes on to explain why the correct answer is 3.4%. Boy, was he wrong! Read the rest of this entry »

Share this:

Variable Annuity: Bad Investment!

Posted on: June 5, 2014

Recently I was approached by two prospective clients. The husband is a very successful entrepreneur and they are also very frugal. As the result of that, they have accumulated substantial wealth – north of $5mm.

Recently I was approached by two prospective clients. The husband is a very successful entrepreneur and they are also very frugal. As the result of that, they have accumulated substantial wealth – north of $5mm.

The only problem? all of that money is in about 28 variable annuities they purchased over the years. In examining these variable annuities, I turned up the following problems:

1. Horrible returns

For each variable annuity, I was able to calculate its annualized return.

Out of the 28 variable annuities, only two have annualized returns above 4%. Seven have annualized returns between 3% and 4%. Six have annualized returns between 2% and 3%. The rest (13 of them) have returns less than 2% including a few that have negative returns. The average annualized return? 2.12%. Not enough to beat inflation!

2. Horrible surrender charges

There is this one annuity they purchased from Jackson National Life in 2007 for $200k; today it has grown to a “value” of $245k, but if they should cash it out, they would only get $221k since there is a surrender charge of $24k. After seven years, there is still a surrender charge of 12%! This is just horrible! Read the rest of this entry »

Share this:

Deep Risk vs Shallow Risk

Posted on: December 24, 2013

Recently, a prospective client of mine sent me an email asking about my thoughts on Bill Bernstein’s new book “Deep Risk.” I have not read the book yet, but I do have my own ideas about deep risk vs shallow risk.

Recently, a prospective client of mine sent me an email asking about my thoughts on Bill Bernstein’s new book “Deep Risk.” I have not read the book yet, but I do have my own ideas about deep risk vs shallow risk.

I define shallow risk as a potential loss that you can recover from and deep risk as a loss that you cannot recover from.

Market volatility, for example, is a shallow risk. It is very visible and it is scary, there is even a TV channel devoted to it. (That TV channel is called CNBC.)

But taking on shallow risk is how you earn your investment keep. Thus, it should not be feared, it should be welcomed.

Now what are the deep risks you should ardently avoid? I can think of three: inflation risk, behavior risk and agency risk.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

When I am approached by a prospective client, the question they always ask without fail is “Are you properly licensed?”

When I am approached by a prospective client, the question they always ask without fail is “Are you properly licensed?”

This is actually the wrong question. The right question should be, “Which license do you have?”

Generally, there are two types of licenses for people who call themselves a “financial advisor.” People who passed the series 65 test and people who passed the series 7 test. The nature of these two licenses are as far apart as heaven and earth.

Series 7 is a securities license. People who have passed this test can legally be a broker. They are actually prohibited by law to give financial advice, except incidental to the financial products they are selling.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

Recently a business owner asked me to review his investment portfolio. He is currently with an Ameriprise financial advisor and his gut feeling tells him something is amiss.

He is paying the advisor 1.6% in fees. First of all, this fee is quite exorbitant. For the size of his portfolio, he shouldn’t be paying more than 1% in advisor fees.

Adding insult to injury, for the fee that he is charging, this advisor puts his money into a collection of very expensive mutual funds like ODMAX.

It is very easy to check the expenses of a mutual fund. I just googled ODMAX and I found out it has a load of 5.75% and an expense ratio of 1.36%. (For those who don’t know, load is a one time charge to pay commision to the Ameriprise advisor who doubles as a broker. Expense ratio is an ongoing annual charge.)

ODMAX is a mutual fund that invests in emerging market stocks. If you use the low cost alternative, aka a Vanguard fund, you will pay no load and the expense ratio is only 0.33%, a saving of 1.06%.

Don’t ever underestimate these tiny savings. Because in ten years, the savings will be more than 10%, in twenty years, more than 20%. This businessman is in his 50s; he can easily live another 30 years. I asked him: “How would you like to be more than 30% poorer in retirement?” That is exactly what this financial advisor will make him.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

The Agony of The Landlord

Posted on: September 5, 2013

A physician client of mine called me the other day and asked my advice as to whether she should evict the tenant currently residing in her condo. This is advice I hate to give. Let me explain.

A physician client of mine called me the other day and asked my advice as to whether she should evict the tenant currently residing in her condo. This is advice I hate to give. Let me explain.The tenant is a single mom with two young children, whose estranged husband just stopped paying child support because he is officially unemployed, but the tenant believes he is getting paid under the table.

My heart goes out to this tenant, I would never want her and her children to become homeless. But my head tells me that if my client lets her stay for free, she would most likely wind up staying for free forever and my client’s rental property would become a toxic asset.

So what should I advise my client?

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

I want all of you to know that not all financial advisors are the same. In fact “financial advisor” is a free term. There is no educational requirement nor legal requisite. Justin Bieber and his grandmother could call themselves financial advisors and begin dispensing advice – and they would not get into trouble for it!

In reality though, there are generally four types of people who like to call themselves “financial advisors”:

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

Morgan Stanley Smith Barney

I went to a Morgan Stanley financial advisor associate recruitment meeting recently to spy on how they train their new financial advisors.

They have an extremely rigorous 36 month program. New associates are expected to pass series 7 and series 66 license testing in the first 12 months. These licenses enable them to charge both fees and (hidden) commissions. (Comparatively, my series 65 license prohibits me from charging commissions.)

As soon as they get the licenses, they are expected to go into “production.” The firm sets very tough production targets. If they fail the targets, they will be kicked out of the program.