Archive for the ‘Annuity and Life Insurance’ Category

A few weeks ago, I told you about Jon, a long-time reader of my newsletter. His Edward Jones financial advisor was trying to sell him a Variable Universal Life (VUL) policy, and he asked me for my 2nd opinion. Instead of writing my opinion, however, I posted his question to my newsletter readers, and asked you guys to make an assessment.

A few of you came back with the answer of YES since the $2mm death benefit is huge, and the annual premium payment of $17k appears to be quite reasonable. On top of that, the buyer gets the flexibility to skip payments as well. I believe this view of the product is exactly what the insurance company wants but it is misguided.

To answer Jon’s question, I first talked to him to determine his family’s actual need for life insurance. He has two teenage kids and he and his wife already both have 20-year term life insurance policies, each with a $2mm death benefit. They clearly have no need for additional life insurance.

Now let’s look at the product itself. A VUL policy is a combination of two components – life insurance and investment. The product is not entirely under the oversight of the SEC, therefore there is a huge regulatory loophole that the insurance company can use to take advantage of the buyers.

Read the rest of this entry »Share this:

Recently, a long-time reader of my newsletter came to me for a second opinion financial review. His current financial advisor from Edward Jones had highly recommended a Variable Universal Life Insurance policy as an awesome investment vehicle for his family.

This reader of mine, I’ll call him Jon, is married with two teenagers. Both are very healthy and will go to college in a few years.

The pitch his advisor made for this product includes: 1) it is very flexible, you can decide when and how much to make the premium payments; 2) you can invest in the stock market through various mutual funds to build up cash value, and 3) with this product, you can achieve tax-free growth of the cash value.

I went over the list of available mutual funds and the one with the lowest expense ratio is the Fidelity VIP 500 Index Fund at 0.35%. About one-third of the funds have an expense ratio higher than 1% however.

For this policy that pays a death benefit of $2mm, Jon needs to pay about $17k per year until he is 70, after that, he can stop paying and the policy will remain valid, according to the policy illustration.

Do you think Jon should buy this VUL policy as an investment or not? If you think the answer is yes, reply and give me three reasons. If it’s no, also give me three reasons. Next week I will share my thoughts.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

A new client of mine asked me to evaluate this situation. Last year, a so-called “financial advisor” who was actually an insurance agent got them to transfer all of their money from TSP (a fantastic retirement plan for federal employees) into an equity index annuity with an insurance company.

The selling points often presented by these “advisors” for products like these are that an index annuity can save them taxes and that the money is protected from market drops and will never go below its original value. The first selling point is bogus in this case! Since the money was in TSP where money grows tax-free anyway. The second selling point appears on the surface to be valid, but it is also bogus as I will show you in a moment.

Read the rest of this entry »Share this:

This is, unfortunately, an all-too-common story I have heard. A new client of mine told me that his father bought a $500k variable universal life insurance policy for him 26 years ago, hoping that when he died he would leave half a million dollars to his children. (26 years ago, that was a lot of money.)

The premium for the insurance policy is $9000 a year. At some point, his dad asked him to take over the premium payments.. Between the two of them, they have already paid in a total of $234,000, but the cash value of the insurance is only $103,000.

Next year, his dad will turn 80 and here is the in-force illustration the insurance company gave him. Basically, even if he continues paying the premium, his insurance will lapse when his dad turns 83, a mere four years from now. If that happens, they will have paid $270,000 to the insurance company, all for nothing. To avoid that outcome, his dad literally has to die in within the next four years.

When his dad turns 80, the mortality expense of the life insurance escalates to $40k – $50k per year, far more than the annual premium. The shortfall has to be drawn from the cash value. That’s why the cash value will dwindle fast. When there is no cash value left, Read the rest of this entry »

Share this:

Long-Term Care Costs

Posted on: September 30, 2015

[by Russ Thornton] At some point, 70% of people over the age of 65 will need some form of long-term care and support.

I get a lot of questions from clients about long-term care insurance.

Yet, I find many people are more willing to discuss their estate planning (and their mortality) than the possibility of finding themselves in a situation calling for long-term care.

Typical objections to insurance for long-term care include:

- It’s too expensive,

- My kids/spouse/family will take care of me,

- I’ll pay for it myself out of my savings and investments,

- or something else.

And let me mention the fact that I don’t sell long-term care or any other type of insurance, so I’m not sharing this information to motivate you to buy something from me.

In fact, long-term care insurance isn’t necessary for many, despite many insurance companies’ and agents’ best attempts to use fear-based tactics to sell you policies. Read the rest of this entry »

Share this:

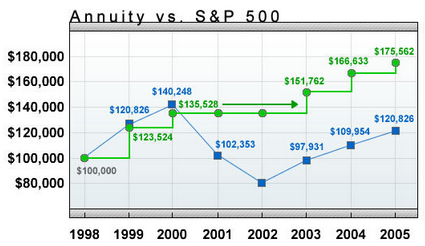

Typical Salesman’s Chart for EIA

Financial author Allan Roth once wrote an article called “Investment Trick – Annuity Style” where he asks a rhetorical question, “If the S&P 500’s total return is 12% in a given year, what do you think your equity index annuity (that is supposed to track the S&P 500) would return”?

- 10%

- 8%

- 5.4%

- 3.4%

Allan Roth goes on to explain why the correct answer is 3.4%. Boy, was he wrong! Read the rest of this entry »

Share this:

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

Recently, we took the money out in favor of a better investment, and boy was she in for a shock! There was a $17k surrender charge and nearly $3.6k in tax withholdings. All the interest she supposedly earned in the annuity went to the surrender charges, and now she has to pay income taxes on that interest!

Here is why a fixed rate annuity is nothing like a savings account.

1. A savings account is FDIC guaranteed, in other words, it has the full faith and credit of the US government behind it. A fixed rate annuity is NOT FDIC guaranteed, it only has the credit of the issuing company behind it. Think AIG! Read the rest of this entry »

Share this:

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Why surrender charges are sunk costs?

Imagine you were sold a $100k variable annuity with a ten year surrender period. The agent who sold you the contract collected a 10% commission, or $10,000. Where do you think this money came from?

Bingo! Your pocket. I hate to break it to you, but insurance companies are not in the charity business and they sure as heck aren’t gonna tell you that 10 of the 100Gs you just handed over to them are going to pay the agent’s commission! If they did that you’d pull your money out and rightly avoid them like the plague in the future.

Share this:

Variable Annuity: Bad Investment!

Posted on: June 5, 2014

Recently I was approached by two prospective clients. The husband is a very successful entrepreneur and they are also very frugal. As the result of that, they have accumulated substantial wealth – north of $5mm.

Recently I was approached by two prospective clients. The husband is a very successful entrepreneur and they are also very frugal. As the result of that, they have accumulated substantial wealth – north of $5mm.

The only problem? all of that money is in about 28 variable annuities they purchased over the years. In examining these variable annuities, I turned up the following problems:

1. Horrible returns

For each variable annuity, I was able to calculate its annualized return.

Out of the 28 variable annuities, only two have annualized returns above 4%. Seven have annualized returns between 3% and 4%. Six have annualized returns between 2% and 3%. The rest (13 of them) have returns less than 2% including a few that have negative returns. The average annualized return? 2.12%. Not enough to beat inflation!

2. Horrible surrender charges

There is this one annuity they purchased from Jackson National Life in 2007 for $200k; today it has grown to a “value” of $245k, but if they should cash it out, they would only get $221k since there is a surrender charge of $24k. After seven years, there is still a surrender charge of 12%! This is just horrible! Read the rest of this entry »

Share this:

10. P2P Lending: A New Asset Class?

10. P2P Lending: A New Asset Class?

9. A Lesson From a Client: Celebrity Business Gone Bad

8. The High Cost of Fee-Based Financial Advisors

7. How Often Do Market Corrections Happen?

6. Captive Insurance: A Business Owner’s Heaven?

5. How I Helped a Client Save $100k in One Meeting

4. Variable Annuity Fees You Don’t Know You are Paying

2. Be Careful When Buying a Condo as a Rental Property

1. Profit from Harry Dent’s Prediction? Think Again

Also see Top Ten in July.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Request White Paper | Request Discovery Meeting

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

I am not a fan of permanent life insurance. Over the years, I have helped many people extricate themselves from costly life insurance policies. Invariably, they were sweet talked into buying these products without any real need.

I am not a fan of permanent life insurance. Over the years, I have helped many people extricate themselves from costly life insurance policies. Invariably, they were sweet talked into buying these products without any real need.

But recently, I’ve actually had to help a client shop for a permanent life insurance policy. They have a child with a potentially permanent medical condition. Of course we hope and pray that he will outgrow his medical problem, as many kids do, but as parents, they must prepare for the worst.

This is one of the few legitimate reasons for using permanent insurance. Other legitimate reasons include to pay for estate taxes, or to facilitate business succession.

Here is the decision process I employed to help my client, bearing in mind that insurance products are not under the purview of the SEC and are usually chock full of hidden costs.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

A few days ago, I interviewed Jim Ludwick using Google+ Hangout On Air (HOA.) This is the first time I’ve interviewed an expert live on air! Feel free to laugh as you watch me stutter and trip over my words left and right.

A few days ago, I interviewed Jim Ludwick using Google+ Hangout On Air (HOA.) This is the first time I’ve interviewed an expert live on air! Feel free to laugh as you watch me stutter and trip over my words left and right.

Jim is the owner of MainStreet Financial, he used to be an agent at NY Life. Now he is a licensed insurance advisor.

I did not waste his appearance and got right down to the nitty gritty. I asked about a client case during the interview. Specifically, this client of mine was talked into 1) buying a universal life insurance inside her defined benefit plan, 2) buying a whole life insurance policy for her young daughter, because “it’s a great investment” according to the agent’s illustration of 8% growth.

I asked Jim three questions:

Share this:

![]() Is a Fidelity Personal Retirement Annuity (FPRA) a good investment?

Is a Fidelity Personal Retirement Annuity (FPRA) a good investment?

A client of mine recently asked me the above question. He is a high-income business owner who makes close to $1m a year and he has used up all of his available tax-advantaged investment vehicles. He is interested in this Fidelity product primarily because it is tax-deferred.

Now let me start out by saying that I love Fidelity. I custody all of my clients’ assets with them. Their advisor support team is fantastic and without Fidelity, I wouldn’t have been able to build my independent wealth management practice. FPRAs are also cheap compared to other variable annuities out there and if you absolutely have to buy a variable annuity, an FPRA is definitely the way to go. But…. I don’t recommend it.

Firm | Youtube | Facebook | Twitter | LinkedIn

Share this:

Last week, I got a panicked phone call from a client of mine, “Michael, my wife bought an annuity a few weeks ago. Now we really regret it. The agent won’t take our call! Can you help us?”

Last week, I got a panicked phone call from a client of mine, “Michael, my wife bought an annuity a few weeks ago. Now we really regret it. The agent won’t take our call! Can you help us?”

I went to their home to examine the annuity contract. It was actually relatively straightforward; for $100k, they will get $456 per month for the next 30 years, beginning three years from now. My client is 71 years old; he will be getting his last payment when he is 104 years old! By then $456 will probably be worth $56 in today’s money. Not what I’d call the deal of a lifetime.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

The reward of a financial advisor

Posted on: January 7, 2013

Recently, a client of mine fell, broke his hip and ended up lying on the floor for 20 hours before he was rescued. I went to visit him in the hospital a couple of times. The good news is: he is out of immediate life-threatening danger. The bad news is: he may be wheelchair bound for the rest of his life.

Recently, a client of mine fell, broke his hip and ended up lying on the floor for 20 hours before he was rescued. I went to visit him in the hospital a couple of times. The good news is: he is out of immediate life-threatening danger. The bad news is: he may be wheelchair bound for the rest of his life.

When John first came to me to seek my help with his personal finance, I looked at his overall financial big picture and was pleased overall. He worked at federal and state jobs and enjoyed good pensions. On top of that, he had a decent investment account.

But there was a gaping hole in his retirement security: he was turning 70 then, was divorced, and his children lived far away. That meant if he were to get sick, nobody would be there to take care of him; he would need to hire caregivers. Right then, I insisted that he buy long-term care insurance.

Share this:

My friend Dan is in the life insurance business. Recently, he shared with me a case in which he helped a client of his (let’s call him John) get $600k out of his term life insurance with life settlement.

My friend Dan is in the life insurance business. Recently, he shared with me a case in which he helped a client of his (let’s call him John) get $600k out of his term life insurance with life settlement.

In case you don’t know what life settlement is, it’s the sale of an insurance policy by the owner to a third party for a price higher than the policy surrender value.

How does this work?