Archive for November 2019

What Kills Investment Returns?

Posted on: November 23, 2019

Last week’s newsletter article “Why It’s Awesome To Have a Loser in Your Portfolio” has proven to be quite controversial. More than a few of my readers emailed me to warn that my Finance professor at Oxford was full of bullshit. Let’s put that aside for now, and consider this question:

If there is an investment that has an average return of 25%, would you invest in it?

If you did not jump in right away, you are a smart investor! Investment A falls 50% in one year and gains 100% the next, giving it exactly a 25% average return. If you invest $1000, however, you make absolutely $0 on this investment. On the other hand, investment B gains 25% in both years, so it also has exactly a 25% average return, but now the gain from $1000 investment is $562.5. You can not pick an investment in isolation of its volatility. Because …

Share this:

Don’t take my word for it, this was covered in my Finance class at Oxford. Let me see if I can get the gist across with a few graphs.

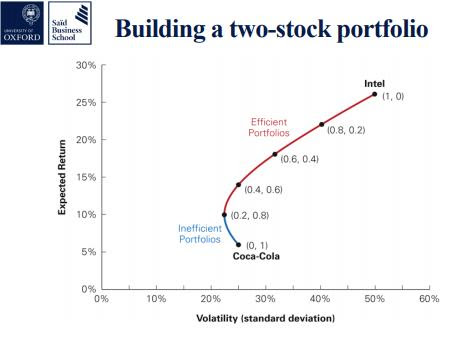

The graph below shows the risk/return profiles of a continuum of two stock portfolios of Coca-Cola and Intel. The vertical axis represents the expected return, and the horizontal axis represents volatility risk.

As you can see, Coca-Cola by itself is a low risk – low return stock, while Intel by itself is a high risk – high return stock. By using different weighting in the two stock portfolios, we can create different risk return trade-offs, represented by the curve. Read the rest of this entry »

Share this:

This happened over the past weekend. A reader of my newsletter signed up for my free 2nd opinion financial review.

This happened over the past weekend. A reader of my newsletter signed up for my free 2nd opinion financial review.

As I went over his 401k investments, I saw that he had invested the entire balance in a target-date fund which normally is a good choice. Upon closer examination, I realized that the target-date fund has an expense ratio of 0.8%. That’s high. I went through the list of available investment options since most 401k plans limit them. I found an S&P 500 index fund, an international stock index fund, and a bond index fund, all with an expense ratio of only 0.05%. I constructed a portfolio made up of these three funds, saving him 0.75% a year. The entire exercise took me around 15 minutes.