The Profitability Premium in Stock Returns

Posted on: June 7, 2018

Ever since Fama and French published their seminal paper “The Cross-Section of Expected Stock Returns” in 1992, the world (at least the academic world) has come to understand that over the long run, small cap stocks outperform large cap stocks and value stocks outperform growth stocks.

This quest to understand stock returns has not stopped. In 2013, Robert Novy-Marx published “The Other Side of Value: The Gross Profitability Premium” in the Journal of Financial Economics. In the course of this research, he discovered that profitability, measured by gross profits-to-assets, has roughly the same power as book-to-market in predicting the cross-section of average returns. Profitable firms generate significantly higher returns than unprofitable firms, despite having higher valuation ratios.

Almost concurrently, other researchers confirmed Novy-Marx’ discovery, notably Fama and French’s new paper “A Five Factor Asset Pricing Model” and Hou, Xue and Zhang’s “Digesting Anomalies: An Investment Approach.” Both papers were published in 2015.

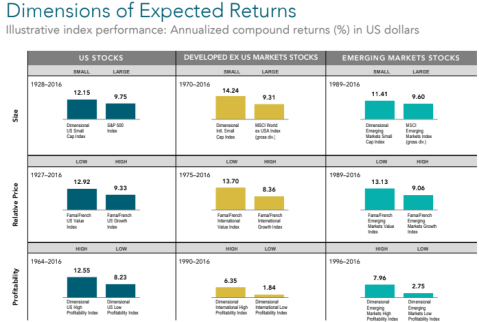

Unlike the small cap premium and value premium, the profitability premium does not have a satisfactory risk-based explanation.

However, to the extent data is available, it is found to be rather persistent and consistent. (See chart below.)

That’s why, Dimensional Fund Advisors, the mutual fund company I use to invest my clients’ money and my own money as well, now implements a profitability filter to overweight profitable stocks.

(Feel free to share if you find it insightful.)

Schedule a Discovery review with me, or get my white paper for free: The Informed Investor: 5 Key Concepts for Financial Success.

Leave a comment