Why It’s Awesome To Have a Loser in Portfolio

Posted on: November 18, 2019

Don’t take my word for it, this was covered in my Finance class at Oxford. Let me see if I can get the gist across with a few graphs.

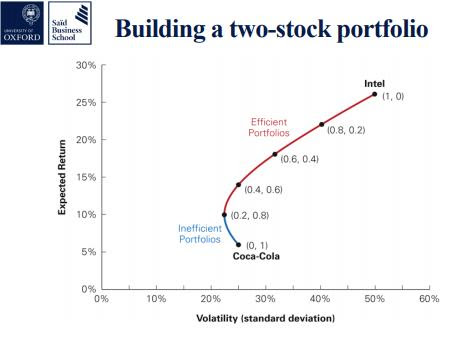

The graph below shows the risk/return profiles of a continuum of two stock portfolios of Coca-Cola and Intel. The vertical axis represents the expected return, and the horizontal axis represents volatility risk.

As you can see, Coca-Cola by itself is a low risk – low return stock, while Intel by itself is a high risk – high return stock. By using different weighting in the two stock portfolios, we can create different risk return trade-offs, represented by the curve.

The curve in blue represents portfolios that are inefficient, meaning for the same level of risk, you can find other portfolios (red curve just above) that deliver higher returns. On the other hand, the curve in red represents portfolios that are efficient, meaning, given a certain risk level, they achieve the highest expected return, or given a certain expected return, it achieves the lowest risk level.

Simply put, in constructing a portfolio, we want to move as “northwest” as possible because “north” means higher returns and “west” means lower risk. Now, here is the real controversy: if we throw a loser into the portfolio mix, will it help move the efficient frontier northwest? It turns out it does!

Bore is a total loser, it has the same level of risk as Coca-Cola, but it has a much lower expected return. Our first inclination is to not include it in our portfolio. But it turns out including Bore in the portfolio moves the efficient frontier from the blue curve to the red curve, thereby creating portfolios that have better risk-return trade-offs! In fact, there is no portfolio of the two winner stocks that can not be beaten by including the loser as far as risk-return concerned.

It’s odd and it’s counter-intuitive, so I asked my professor in class: “How can I convince my clients who don’t know these formulas that it’s awesome to include a loser in their portfolio?” The professor chuckled and said: “Tell them it’s the magic of diversification.” I am not sure if you are convinced, but mathematically, he is right.

Schedule a free 2nd opinion financial review, buy my wealth management books on Amazon, or download the pdf version here.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Leave a comment