Another Example of Return and Volatility Manufacturing

Posted on: July 25, 2021

Last week I shared an example of how you could still lose money on an investment that gives you a 20% average annual return. I ended the article with five questions:

- Can the average return tell you if you will make or lose money?

- Can the average return tell you how much money you make or lose?

- What else determines if you make or lose money?

- Why do hedge funds love to use average returns?

- Why do I use asset class diversification to reduce client portfolio return variability? (Note that this will make the return number look smaller.)

Here are the right answers:

- No.

- No.

- Return variability or volatility. It is also called volatility drag – the higher the volatility, the lower the return. Here is an article on this subject I wrote 13 years ago.

- It’s great for marketing.

- One word: I am a fiduciary. (Ok, four words.)

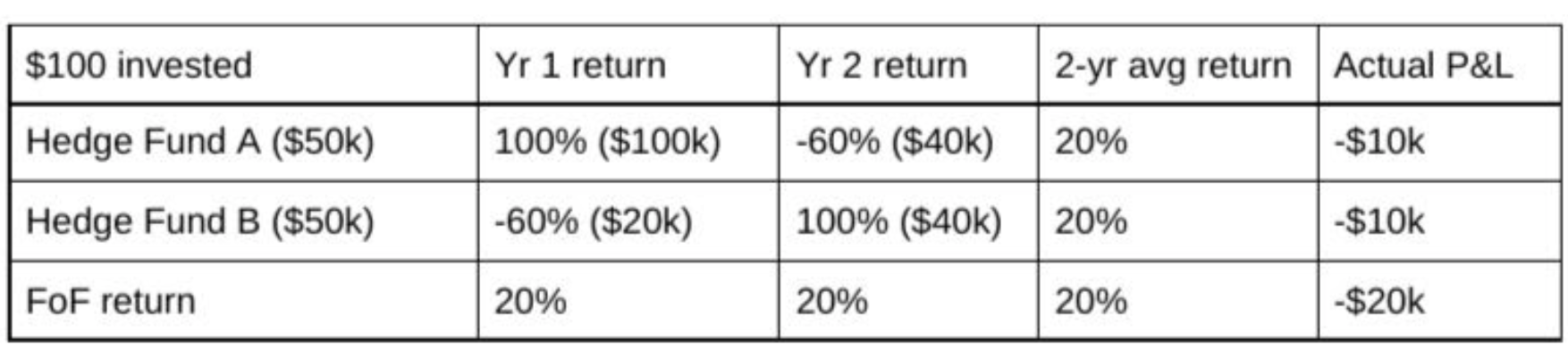

Today I am going to illustrate for you that even return variability can be manufactured. A fund of hedge funds (FoF) claims to be extremely good at picking winning hedge funds. They invested in Hedge Fund A and Hedge Fund B in the last two years and made a 20% average return every year, without any year-to-year variability. With such stable returns, you’ve got to make money right? Not so, once again you lost close to 50% of your money after fees.

Let’s assume you invested $100k into the FoF and the FoF split your money into Hedge Fund A and Hedge Fund B evenly, that is $50k each. After two years, both hedge funds have only $40k left. That is, each fund lost $10k so the FoF lost a total of $20k. The FoF will still report that they deliver a 20% return every year. According to them, not only is the return outstanding, but also they did it without any volatility. This makes for great marketing. The original investors may leave in disappointment, but a new set of investors will happily give money to them.

Now, all of this assumes the hedge funds and FoF do not charge fees, but in reality, all of them charge a fee of 2% plus a 20% carry. So the loss to the investor is much deeper. Here are my back of envelope calculations.

So the investor not only lost $20k of their initial investment, but they also lost another $26.8k to the fees charged by the three funds.By the end of the 2nd year, the investor will get back only $53.2k out of his $100k investment despite the FoF’s 20% average annual return without volatility!

That’s why I always advised against investing in unregulated private funds you don’t understand and have no control over. David Swensen, Yale’s Endowment CIO, called these private funds a wealth transfer mechanism from the merely wealthy (qualified investors) to the ultra wealthy (fund managers and sponsors.)

Schedule a 2nd opinion financial review, buy my wealth mgmt books on Amazon.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Leave a comment