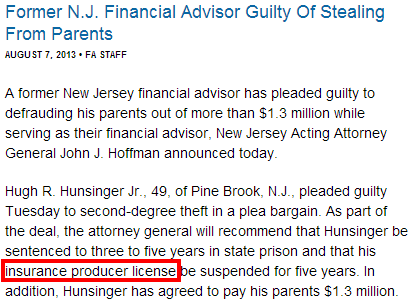

Posts Tagged ‘insurance agent’

I want all of you to know that not all financial advisors are the same. In fact “financial advisor” is a free term. There is no educational requirement nor legal requisite. Justin Bieber and his grandmother could call themselves financial advisors and begin dispensing advice – and they would not get into trouble for it!

In reality though, there are generally four types of people who like to call themselves “financial advisors”:

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

A few days ago, I interviewed Jim Ludwick using Google+ Hangout On Air (HOA.) This is the first time I’ve interviewed an expert live on air! Feel free to laugh as you watch me stutter and trip over my words left and right.

A few days ago, I interviewed Jim Ludwick using Google+ Hangout On Air (HOA.) This is the first time I’ve interviewed an expert live on air! Feel free to laugh as you watch me stutter and trip over my words left and right.

Jim is the owner of MainStreet Financial, he used to be an agent at NY Life. Now he is a licensed insurance advisor.

I did not waste his appearance and got right down to the nitty gritty. I asked about a client case during the interview. Specifically, this client of mine was talked into 1) buying a universal life insurance inside her defined benefit plan, 2) buying a whole life insurance policy for her young daughter, because “it’s a great investment” according to the agent’s illustration of 8% growth.

I asked Jim three questions:

Share this:

A client of mine is trying to get his money out of an ill-conceived investment. I want to share this with you so you don’t make the same mistakes.

A client of mine is trying to get his money out of an ill-conceived investment. I want to share this with you so you don’t make the same mistakes.

In 2009, he had a windfall of $1m. He asked a lady who had sold him a bunch of annuities where he should put his newfound cash. He further told her he was already up to his neck in annuities so he wanted to take some risks.

The agent pointed him to a celebrity business. Basically, some hollywood celebrity was trying to start an online gaming business, and needed $30m to do so.

My client went to their presentation and was mesmerized by the income projection. Then, when he saw that one of his relatives was a minority partner in the venture, he was totally sold. He signed a check for $1m on the spot.

He might as well have flushed it down the toilet.

Here is what he did wrong.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

A Balanced Portfolio to Avoid (III): Most Financial Advisors Are Not Fiduciaries!

Posted on: April 30, 2011

My friend is a savvy businessman. However, like most Americans, he has a misconception: he thinks financial advisors are legally bound to put clients’ interests first. This can not be further from the truth. Everybody and his grandma can be a “financial advisor.” Unlike being a “physician”, there are neither legal requirements no educational qualifications. Whether a certain financial advisor is bounded legally to act in his client’s best interests all depends on his true profession. Here is an ad hoc summary:

| Professional Title | Fiduciary? |

| Attorney | Yes |

| Certified Public Accountant (CPA) | Yes |

| Registered Investment Advisor (RIA) | Yes |

| Financial Planner | Maybe |

| Certified Financial Planner (CFP) | Maybe |

| Wealth Manager | Maybe |

| Insurance Agent | No |

| Registered Representative | No |

| Stock Broker | No |

Share this:

You may not believe it: the term “financial advisor” is a free title. Anybody can use it; there is no legal requirement, nor educational qualification. In practice, though, generally there are three types of people who use this title: insurance agents, stockbrokers, and registered investment advisors (RIAs). Whether they are required to disclose fees all depends on what type they are.