Posts Tagged ‘bad investment’

Typical Salesman’s Chart for EIA

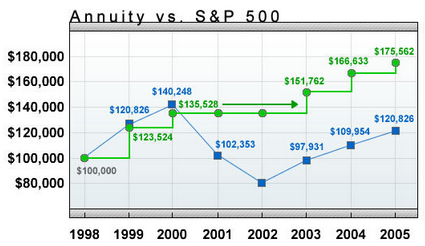

Financial author Allan Roth once wrote an article called “Investment Trick – Annuity Style” where he asks a rhetorical question, “If the S&P 500’s total return is 12% in a given year, what do you think your equity index annuity (that is supposed to track the S&P 500) would return”?

- 10%

- 8%

- 5.4%

- 3.4%

Allan Roth goes on to explain why the correct answer is 3.4%. Boy, was he wrong! Read the rest of this entry »

Share this:

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

Recently, we took the money out in favor of a better investment, and boy was she in for a shock! There was a $17k surrender charge and nearly $3.6k in tax withholdings. All the interest she supposedly earned in the annuity went to the surrender charges, and now she has to pay income taxes on that interest!

Here is why a fixed rate annuity is nothing like a savings account.

1. A savings account is FDIC guaranteed, in other words, it has the full faith and credit of the US government behind it. A fixed rate annuity is NOT FDIC guaranteed, it only has the credit of the issuing company behind it. Think AIG! Read the rest of this entry »

Share this:

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Why surrender charges are sunk costs?

Imagine you were sold a $100k variable annuity with a ten year surrender period. The agent who sold you the contract collected a 10% commission, or $10,000. Where do you think this money came from?

Bingo! Your pocket. I hate to break it to you, but insurance companies are not in the charity business and they sure as heck aren’t gonna tell you that 10 of the 100Gs you just handed over to them are going to pay the agent’s commission! If they did that you’d pull your money out and rightly avoid them like the plague in the future.

Share this:

A client of mine is trying to get his money out of an ill-conceived investment. I want to share this with you so you don’t make the same mistakes.

A client of mine is trying to get his money out of an ill-conceived investment. I want to share this with you so you don’t make the same mistakes.

In 2009, he had a windfall of $1m. He asked a lady who had sold him a bunch of annuities where he should put his newfound cash. He further told her he was already up to his neck in annuities so he wanted to take some risks.

The agent pointed him to a celebrity business. Basically, some hollywood celebrity was trying to start an online gaming business, and needed $30m to do so.

My client went to their presentation and was mesmerized by the income projection. Then, when he saw that one of his relatives was a minority partner in the venture, he was totally sold. He signed a check for $1m on the spot.

He might as well have flushed it down the toilet.

Here is what he did wrong.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter