Shopping for Permanent Life Insurance for A Client

Posted on: August 31, 2013

I am not a fan of permanent life insurance. Over the years, I have helped many people extricate themselves from costly life insurance policies. Invariably, they were sweet talked into buying these products without any real need.

I am not a fan of permanent life insurance. Over the years, I have helped many people extricate themselves from costly life insurance policies. Invariably, they were sweet talked into buying these products without any real need.

But recently, I’ve actually had to help a client shop for a permanent life insurance policy. They have a child with a potentially permanent medical condition. Of course we hope and pray that he will outgrow his medical problem, as many kids do, but as parents, they must prepare for the worst.

This is one of the few legitimate reasons for using permanent insurance. Other legitimate reasons include to pay for estate taxes, or to facilitate business succession.

Here is the decision process I employed to help my client, bearing in mind that insurance products are not under the purview of the SEC and are usually chock full of hidden costs.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Mutual Companies

Insurance companies are organized as either a mutual company or a stock company.

With the mutual structure, policyholders are also owners of the company. This is a marked difference from the stock structure, whereby policyholders are merely customers, and managers are supposed to maximize profits for stockholders, at the expense of customers.

By limiting my selection to mutual companies, I eliminated one layer of conflict of interest.

Using this criteria, we narrowed it down to three companies: Northwestern Mutual, Mass Mutual and New York Life.

Product Simplicity

There are many types of permanent insurance: whole life, universal life, variable universal life and equity indexed life, just to name a few.

The more complicated the product, you can be sure the more costs are hidden in nooks and crannies. So I advised my client to go for the simplest of all – fixed premium whole life.

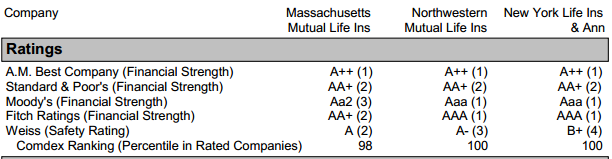

Company Strength

With permanent life insurance, you are literally entrusting your life and death to a company. And you sure hope it can last as long as your life. One can not just pick a life insurance policy without examining the company’s financial strength. All three companies are very strong financially, as illustrated by the table 1 below.

Investment Performance

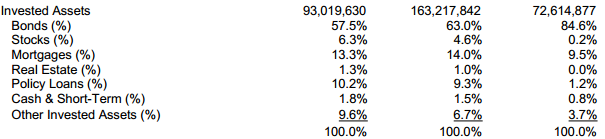

This part is usually the favorite of insurance salesmen, but it is not as important as other points above. Part of the reason they like to talk about it is because they can legally show illustrations that bear little resemblance to reality.

Since my client insisted on knowing, I examined the investment assets of all three companies. It turns out, not surprisingly, they invest largely in the same way: in various fixed income securities, and a teensy tiny bit of stocks, see table 2 above.

Upon closer examination, Mass Mutual’s portfolio has more exposure to duration risk and equity risk. I thereby concluded Mass Mutual will earn a slightly higher return than that other two.

This is straight out of ‘modern portfolio theory’ and there is no mystery. Duration risk and equity risk are compensated risks, the more risks you take, the more returns you earn.

Request White Paper | Request Discovery Meeting

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

2 Responses to "Shopping for Permanent Life Insurance for A Client"

2 | Michael Zhuang

September 2, 2013 at 10:48 pm

Incidences like this happened far so often it is criminal. But Congress is doing nothing because all of them need financial industry’s money to run re-election, so they are doing their best to moth-balling fiduciary standard.

I usually tell me clients if you don’t have $5mm and above and most of it are in fixed assets, don’t worry about paying estate taxes.

September 2, 2013 at 8:47 pm

My mother was sold an insurance policy to “protect her against estate taxes”. The agent never even asked what was her net worth. My mother never asked for advice from a disinterested third party, because she thought the agent was giving her advice. Her kids are all grown up and her net worth is well below the level estates are taxed, so the policy was essentially useless except to make money for the agent and insurance company. It was clearly a marketing tactic, a believeable excuse for a sale to a naive buyer, a.k.a. a plausible lie. There are few legitimate reasons for buying a permanent insurance policy (instead of term), and even fewer people to whom it applies. Caveat emptor, indeed.