Triffin’s Dilemma: The Privilege and The Curse of the Dollar As World Currency

Posted on: March 28, 2025

Following our series about academic research, today I will write about Triffin’s Dilemma, a theory proposed by Dutch economist Robert Triffin in the 1960s.

The theory postulates that the country that owns the world’s reserve currency will inevitably face a persistent trade deficit that will imperil the confidence in that currency.

The theory was originally tied to the Bretton Woods Accord after World War II, where the US dollar was pegged to gold, and the rest of the world’s were pegged to the dollar. In 1971, President Nixon announced the de-pegging of the dollar from gold, effectively, making the dollar a fiat currency that the government could “print” as much of as they wanted.

This is an exorbitant privilege that other countries do not enjoy. By this, I mean that no matter what problems our country faces, we can print our way out of trouble. The oversupply of the dollar would normally cause hyperinflation in our country, but since ours is the world currency, we can export our surplus dollars to the rest of the world by running a trade deficit.

Exporting dollars is a great business to have, since instead of goods, which requires costly manufacturing, dollars can be created by simply adding an entry into the Fed’s computer system. However, a side effect is, that nobody wants to invest in manufacturing and no young people want to work in factories. All smart kids want to be in finance, the industry that is closely related to money creation, allocation, and management. This has led to overfinancialization and the gradual deindustrialization of the country (See chart below.)

Read the rest of this entry »Share this:

Continuing the streak of writing about the most prominent academic research papers on finance and investment, today I will write about “Returns to Buying Winners and Selling Losers,” which was published in 1993 in the Journal of Finance and is currently the third most highly quoted paper in history.

The authors, Narasimham Jegadeesh and Sheridan Titman, studied whether there is persistent money to be made by buying winners and selling losers, otherwise known as the momentum strategy. If the answer is yes, what is the best way to execute it?

They found that if one buys a portfolio of winners (stocks with the top decile returns in the previous 12 months) and sells a portfolio of losers (stocks with the bottom decile returns in the previous 12 months), and holds that for 3 months, one can achieve a return of 1.49% per month on paper. This is huge! This level of monthly returns translates into nearly 18% annual return.

Throughout my 20 years of giving financial advice, I have noticed that amateur investors love momentum strategy, while more mature investors shun it because they have learned the caveats.

So what are the caveats?

Read the rest of this entry »Share this:

How To Pick Mutual Fund Winners

Posted on: January 27, 2025

In answer to my readers’ response to my survey last year, I will be writing a series of articles about academic research in the realm of finance, focusing on studies that are pertinent to us, the average investor.

Today, I am writing about the most cited research in the Journal of Finance. It’s written by Mark M. Carhart, and titled “On Persistence in Mutual Fund Performance”, published in 1997.

Why should you care?

Well, if the research were able to help us identify a few persistent winners among the more than 10,000 available funds, wouldn’t that make our investment life a lot simpler? We could hold only the winners and be done with it. Unfortunately, the research did not find any persistent winners. More precisely, other than a small momentum effect, the research found no evidence that any mutual fund has the ability to consistently outperform the market.

However, the research did find that mutual fund expenses and transaction costs are persistent predictors of underperformance. A 1% increase in expense ratio correlates to a 1.5% decrease in fund performance and a 1% increase in fund turnover results in a 0.95% decrease in fund performance.

Here are the three expenses or costs that you should especially watch out for.

Read the rest of this entry »Share this:

How to Be A Resilient Investor

Posted on: January 12, 2025

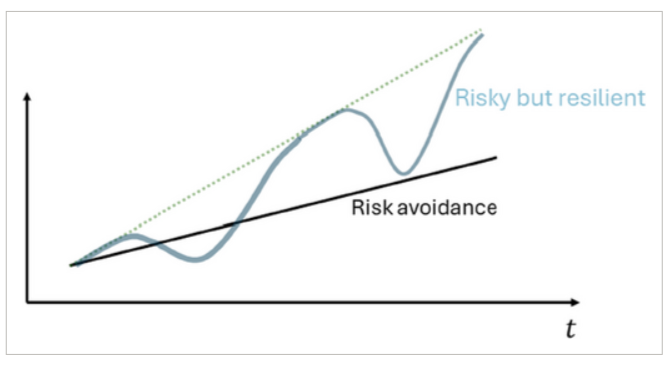

Recently, Markus Brunnermeier, the president of the American Finance Association, gave a presidential address titled “Macrofinance and Resilience”. In this address, he introduced the concept of resilience, which he distinguished from risk. He admonished finance researchers and practitioners to change their focus from risk management to resilience management.

He defined resilience as systematic positive reactions to negative economic shocks. He used the following chart to illustrate the effect of resilience vs. risk avoidance.

Put into layman’s terms, if you are financially resilient, you can potentially take on more risk and earn higher rewards.

The concept of resilience can be applied to many areas, from personal finance to investing. Today let’s focus on investing and ask ourselves what it takes to be a resilient investor. Financial resilience has a much broader scope and will be covered in my next article.

I’d like to suggest a four-point approach to being a resilient investor:

Read the rest of this entry »Share this:

This article was forwarded to me by a client of mine. It was written by Mr. David Karp, who asked seven questions regarding one’s relationship with their advisor. These are excellent questions! I will repost Mr. Karp’s questions and responses, along with my own answers in red and bold.

Besides our family members and close friends, few relationships in life are as important as that of client and wealth advisor … and long lasting. After all, your wealth advisor is trusted with the financial well-being of you and your family, hopefully for generations to come. A good wealth advisor does much more than just manage your investments. He or she will get to know you and your family, your hopes and dreams and the legacy you want to leave. It’s a holistic approach that should be wholly based on the best interests of you and your family.

So how do you evaluate a wealth advisor to ensure you partner with someone who can provide the comprehensive, yet highly individualized set of solutions you need and deserve? Below are seven questions to ask prospective wealth advisors:

Read the rest of this entry »Share this:

- In: Life

- Leave a Comment

The eBook version of my book “Entrepreneur Wealth Management Made Easy” is now free! on Amazon for the next three days. Go get it: https://shorturl.at/xKa8z

Note that Amazon will try to lure you into subscribing to their KindleUnlimitedwith the first big yellow button “Read for Free”, avoid that. Click the second deeper yellow button “Buy now with 1-click” instead.

This is my New Year gift for all entrepreneurs out there. Please forward to your entrepreneur friends.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

US Elections and Stock Returns

Posted on: November 3, 2024

Some readers of my newsletter asked me how to position their investments for the upcoming election.

I did a survey of academic journals on this topic, however there are basically no research papers available. There is an article published in the Journal of Financial Analysis, but this journal is not considered a top-tier academic journal. The lack of research could either mean that this topic is not viewed as a serious academic topic, or that there is simply not enough data to establish any validity.

I then went on to research industrial publications and found an interesting chart to show to you, my readers, that will drive home an important point that is dear to me, specifically, that you shouldn’t try to outsmart the market based on presidential politics.

See the chart below, during the Trump administration, renewal energy stocks outperformed traditional energy stocks by 43%; during the Biden administration, renewal energy stocks underperformed traditional energy stocks by 53%. If you had picked stocks based on presidential preferences, you would have been screwed left and right, literally.

Read the rest of this entry »Share this:

- In: Life

- Leave a Comment

Thank you so much to everyone who responded to my recent request for your opinions. Let me cut to the chase: 45% of you want me to write about the latest academic research; 36% want to hear about cautionary tales, and 19% want both – one person even suggested that I should be able to combine the insights from academic research with cautionary tales.

Cautionary tales are relatively easy to write since they are direct results of f my work with my clients. I often deal with things they did before I started working with them or things I wish they had discussed with me before acting.

It is much more challenging to write about academic research. Most academic papers are very abstract and they are scattered throughout various journals. I must first survey these journals and extract useful insights from them.

If writing a cautionary tale is an 1-hour job, writing about academic research could take 10 hours. But I will do that since that’s what you have asked me to do. And, quite frankly, writing about these studies will help me better manage my clients’ wealth.

Here are the journals that I will survey:

Read the rest of this entry »Share this:

Loyal readers of my newsletter may have noticed that I haven’t written a newsletter article for over a month. This pause has given me time to think about what I should write about the remainder of this year and next year. It has come down to two broad topics, and I’d like my readers to help me decide.

Some of you may know that I have published two books. The first one, Physician Wealth Management Made Easy, was published in 2017, the second one, Entrepreneur Wealth Management Made Easy, in 2019. In these books, I use real-life cautionary tales to teach useful financial lessons. Since the publication of these two books, I have heard five more years worth of cautionary tales from folks who came to me for advice. I think my readers can learn a lot from these tales. What do you think?

Read the rest of this entry »Share this:

If your Financial Advisor has Conflicts of Interest: Three Quick Ways to Determine

Posted on: September 6, 2024

In my last newsletter, I wrote about finding $50k+ worth of hidden costs due to conflicts of interest, and a reader asked me if there is a quick way to check if her financial advisor has such conflicts. Her question inspired my article today.

Before we dive into that, I must first give you a quick overview of the legal environment in which financial advisors operate. There is the Securities Exchange Act that regulates brokers and does NOT require them to act in the best interest of their clients, and there is the Investment Adviser Act that regulates RIAs (registered investment advisors) which does require them to act in the best interest of their clients.

Your financial advisor can be a broker, an RIA, or even dually registered. Those dually-registered ones can be especially deceptive. Here is an actual example – the last few lines of a financial advisory firm’s website:

Read the rest of this entry »Share this:

This morning, I did a portfolio review for a 2nd Opinion Review customer. It is a portfolio worth just under $4mm and I found $56k of hidden costs per year.

Load is the least hidden of all hidden costs, it is a one-time charge that happens when the broker (“financial advisor”) puts your money in a mutual fund. The mutual fund immediately takes a percentage of your money and gives it to the broker as commission. Since this is too obvious, few brokers are that blatant these days.

Expense ratio is the percentage the fund deducts from your investment, and part of this deduction is given to the broker as a kickback. It is even more costly since it occurs every year. It creates an adverse incentive, since the broker is more inclined to put your money in funds that give them a higher kickback. The gold standard of expense ratio is 0.05%. Note that many funds in this analysis have an expense ratio over 1%, over twenty times more expensive than the gold standard.

Turnover measures how frequently the fund manager churns your investments. The more frequent the churn, the more money you lose and the more money the brokerage that handles the trades makes. The gold standard of turnover is less than 10%. If a fund has more than 100% turnover, it belongs in the category of horrible, since 100% equates about 1.2% loss of return.

See below the result of the portfolio review. Numbers in yellow are bad, numbers in red are outright horrible. Compare these numbers to the numbers in green, which is our gold standard.

Read the rest of this entry »Share this:

What has happened in the last few days was a mad dash out of the door of all US dollar-dominated assets to buy back Japanese Yen. Why so? I have to start by explaining the Yen carry trade.

For a long time, Japan’s Central Bank has maintained an extremely low interest rate policy of between 0% and 0.1%. If you were smart money with the right access, what would you have done to earn effortless money? You would borrow Japanese Yen and convert it to US dollars. By just investing the money in US treasuries, you could immediately earn more than 5%. This is called the Yen carry trade, essentially an arbitrage of the interest rate differentials of the US and the Japanese Central banks.

In any event, the result of the Yen carry trade has been the almost endless depreciation of the Japanese Yen, the appreciation of the US dollar, and an endless supply of additional liquidity to the US stock market despite the Fed’s tight money policy. This additional liquidity pushed up all manner of asset prices. But alas, all good trade has to come to an end.

Read the rest of this entry »Share this:

Last week I published a newsletter article titled “Will The Stock Market Return to The Fundamental?” I have received a good number of responses, and as promised, today I will share my thoughts.

The traditional economic theory has always presumed that economic actors are calculating and rational. The application of this presumption in the investment field is the efficient market hypothesis, which basically says that investors rationally pay the prices for expected future earnings adjusted for risk. The biggest proponent of the efficient market hypothesis is Nobel Prize winner Eugene Fama.

The efficient market hypothesis has its biggest opponent in Robert Shiller, who years ago published his seminal work that illustrated how a 1% change in dividends can oftentimes result in a 15% change in the stock price. If investors are, in fact, calculating and rational, stock prices shouldn’t fluctuate so much relative to dividends.

Read the rest of this entry »Share this:

The title of this article comes from a recent discussion I had with a client of mine. First, we should define what “the fundamental” means. It is best defined in Intelligent Investor, a book by Warren Buffet’s teacher Benjamin Graham. In short, his idea of a good investment is a stock with good earnings selling at a cheap price.

Graham’s insights were lately confirmed by Eugene Fama’s Nobel Prize-winning research, where Fama found that throughout history (until maybe 2015,) small-cap value stocks performed the best.

At present, the stock market in the US is definitely not following Ben Graham’s fundamentals. 70% of all returns are concentrated in the seven biggest tech stocks, all of which are very expensive. Nvidia for example, has a $3T valuation, which is 4 times the GDP of Taiwan, where its AI chips are made.

Read the rest of this entry »Share this:

I asked you all this question yesterday, and today I will share select replies followed by my comments on the matter.

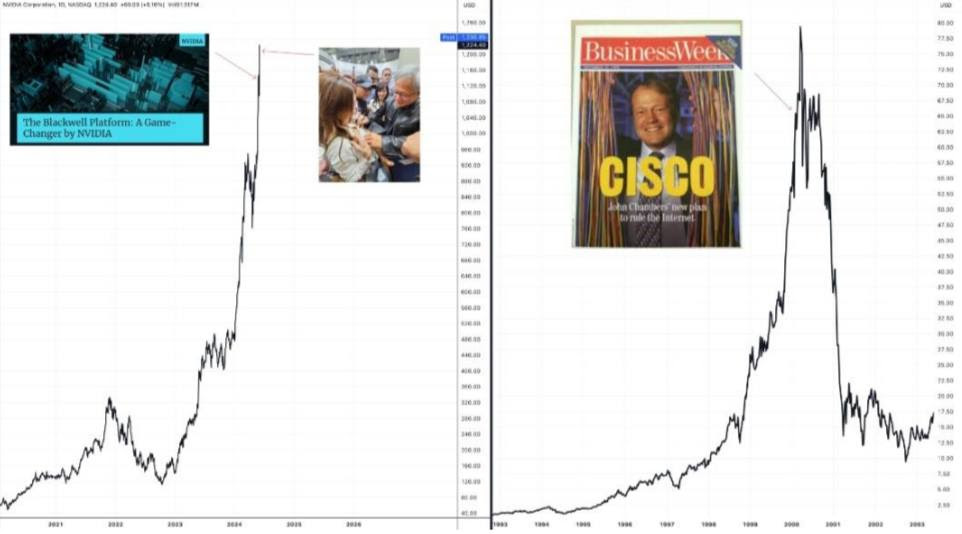

JG wrote: The joy ride will eventually end. The current price dictates an annual revenue growth of 10 percent per year for the next 100 years. This isn’t happening. Ultimately, the dream will fade, and many will lose their money.

JG also shared the chart below. What CSCO was for the internet age, NVDA is for the AI age, namely, an infrastructure provider. This picture is indeed worth a thousand words.

Share this:

Should We Buy NVIDIA Stock?

Posted on: June 23, 2024

In the last few days, I have gotten a few client calls about this. On top of that, my teenage son asked me the same question, telling me a classmate of his had bought this stock and made a few thousand dollars. Instead of answering this question outright, I’d like to hear your views. Please reply to this email, tell me what you think and give me your explanation.

In the next email, I will share with you not only my thoughts but also give you a summary of how you, my newsletter subscribers, responded.

Get informed about wealth building, sign up for The Investment Scientist newsletter