I jumped out of my chair in delight when I learned that Eugene Fama and Robert Shiller had won this year’s Nobel Prize in Economics. These are two economists that greatly influenced my investment philosophy and their works have been an integral part of how I help my clients build and preserve wealth.

Let me explain their contributions:

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

When I was in California, I had a very intelligent debate with a doctor. He mentioned that in 2012, the US took in $2.5T in revenue and spent $3.6T in government expenditures.

When I was in California, I had a very intelligent debate with a doctor. He mentioned that in 2012, the US took in $2.5T in revenue and spent $3.6T in government expenditures.

He accurately pointed out, “If I spent like that, I would be bankrupt in a few years.” He believes so strongly that the US is going the way of national bankruptcy that he has moved substantial amounts of his money overseas and has invested a great deal in gold.

I happen to believe that gold is the most unproductive of assets, since it does not generate dividends or interest and it actually costs money for upkeep in a safe in a Singapore bank.

On top of that, by throwing so much money into gold, one could over prepare for a disaster that is very unlikely to happen and thereby miss out on all the opportunities to grow wealth in this country.

But I still need to explain why the US won’t go bankrupt anytime soon. Here are two explanations:

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

Life: Our Real Treasure

Posted on: October 7, 2013

- In: Life

- Leave a Comment

My wife came home very sad today.

My wife came home very sad today.

A colleague of hers got a call from her son’s teacher. He had come up to her to complain about chest pain when he suddenly collapsed right there in front of her.

My wife’s colleague ran to the emergency room only to find that her son was already pronounced dead. Doctors there couldn’t figure out how this could have happened to a healthy ten year old.

The child’s mother had refused to give up and gave CPR to her lifeless son for an hour until his rib cage nearly cracked.

My wife and her colleague used to swap stories about their respective children regularly and this son was the one she talked about most often. Now he is gone.

I don’t know her, but my heart is overwhelmed by sadness and I am reminded yet again that money and material trappings mean nothing. Life alone is the real treasure.

Share this:

10. How Often Do Market Corrections Happen?

9. Why Asset Class Diversification is Superior

8. Happiness That Doesn’t Take Money

7. Would You Buy This Variable Annuity with Income Guarantees?

5. The High Cost of Fee-Based Financial Advisors

4. Variable Annuity Fees You Don’t Know You are Paying

2. Profit from Harry Dent’s prediction? think again

1. Be Careful When Buying a Condo as a Rental Property

Also see Top 10 in August

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Get my white paper: The Informed Investor: 5 Key Concepts for Financial Success.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

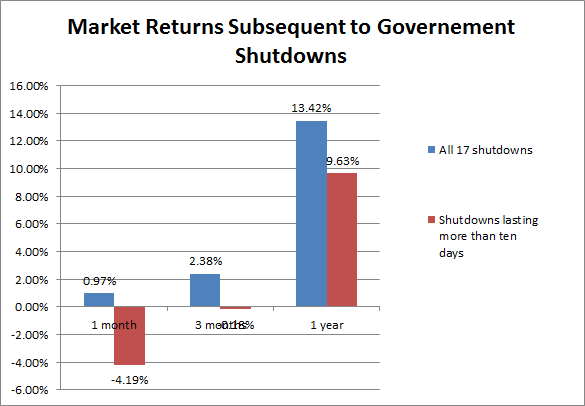

Using the closing price prior to the day of government shutdown as a base line, he found on average, the market rose 0.97% in one month, 2.38% in three months and 13.42% in a year.

If we isolate the 5 most severe shutdowns that lasted more than 10 days, the picture is a bit worse, but not by much. On average the market fell 4.19% in one month, fell .18% in three months and rose 9.63% in a year.

These historical precedents confirm my gut feeling that a government shutdown is really no big deal, as far as the market is concerned.

More worrisome is the upcoming debt ceiling fight. There is no precedent of US default to guide my outlook on this, but the longer the government shutdown lasts, the deeper heels get dug in by both parties and the more likely a default. Nevertheless, I’m still thinking that will also be a storm in a tea cup.

The bottom line is these are issues beyond our control, there is no point worrying about them. If worst comes to worst (ie default,) and the market should drop 20%. That’s actually great because then we can buy shares at a discount!

Share this:

Overwhelmed by Tasks?

Posted on: October 1, 2013

If you are successful in your line of work, you are probably overwhelmed by tasks and find yourself wishing there were 25 hours in a day and 8 days in a week.

If you are successful in your line of work, you are probably overwhelmed by tasks and find yourself wishing there were 25 hours in a day and 8 days in a week.

Well, that wish will not be granted, at least not by me. But there are ways to make those tasks less overwhelming. I call it ‘The Five Ds’: Delete, Do Now, Delay, Divide, Delegate. Let’s go through them one by one.

Delete

Tasks that add no value, just delete them. When I first started out in my career, I used to write a weekly investment column for a local Chinese newspaper. After a whole year of writing, I did not get a single decent client. That task has now been relegated to my delete bin.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

Many middle aged Americans are caught between a rock and a hard place financially. They are the so-called sandwich generation, having to take care of both kids and parents at the same time.

Many middle aged Americans are caught between a rock and a hard place financially. They are the so-called sandwich generation, having to take care of both kids and parents at the same time.

This has recently been a subject of discussion with clients of mine. They are a self made millionaire couple. their parents however, are relatively poor. They have enough to live on by themselves, but if they ever got sick, they would be financially dependent on their children for care.

To that end, my clients have set aside $1m just in case.

I suggested they fork over a few hundred a year to pay for their parents’ gym memberships. If their parents actually use the memberships, my clients may never need to spend the million.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

- In: Life | Wealth Management

- 2 Comments

I visited Dr. Chu who is a family doctor with a solo practice. He told me EHR is killing him.

I visited Dr. Chu who is a family doctor with a solo practice. He told me EHR is killing him.

He is in his 60s, very comfortable with pen and paper, but now Medicare requires him to record all patients’ records electronically, or he will have to pay a stiff penalty.

So now, in addition to seeing patients for eight hours, he has to spend three hours inputting health records.

I sat down with him and we toyed around with a few potential solutions.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

Seven years ago when I started my advisory practice, I used to call myself ‘The Investment Scientist’ to differentiate from those run of the mill financial advisors.

Seven years ago when I started my advisory practice, I used to call myself ‘The Investment Scientist’ to differentiate from those run of the mill financial advisors.

My blog was called ‘The Investment Scientist’, and in marketing materials, I highlighted my academic training and scientific approaches toward investing.

Then, for whatever reason, I stopped doing that. Even the title of my blog has been changed to ‘The Investment Fiduciary.’ (The word ‘fiduciary’ signals my intention to put my clients’ interest first, but few understand its true meaning.)

Over the past year, I’ve rarely heard people call me an investment fiduciary, but sometimes would come across a long lost contact who’d say, “Aren’t you the Investment Scientist?”

There is a lesson here for me. Don’t use obscure words people don’t understand in marketing.

So why am I reverting back to ‘The Investment Scientist’ again?

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

- In: Life

- Leave a Comment

Last Monday I went to Philadelphia to visit a client. After the meeting, I thought I would give myself a break. I would go check out a storytelling contest organized by First Person Arts at the World Cafe.

Last Monday I went to Philadelphia to visit a client. After the meeting, I thought I would give myself a break. I would go check out a storytelling contest organized by First Person Arts at the World Cafe.

When I got there, they asked me if I wanted to participate. Well, I did not have a story, but what the heck, I’d come this far already. I would make up one on the fly. It would be a thrill to take part in a contest totally unprepared.

I spent the next hour preparing a story, which is based on a real-life experience that I’ve kept a secret thus far.

I went on stage, and the crowd loved my story! There was laughter like every ten seconds. In the end, I won the contest hands down. Now, I am a top ten storyteller in Philadelphia! I will have to go back to contest for the title of “Best Storyteller in Philly.”

I was so thrilled by my win, the excitement didn’t even subside after a whole week. This was a seriously cheap thrill, since all in all I’d spent only $10.

Let me elaborate on exactly why I am so thrilled.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

How to Pay Off Debts

Posted on: September 12, 2013

A client I visited shared with me that he is very burdened by his debts. He has a primary mortgage, a secondary mortgage and a personal loan. He asked me whether he should pay off the debts and in what sequence. That’s a fantastic question.

A client I visited shared with me that he is very burdened by his debts. He has a primary mortgage, a secondary mortgage and a personal loan. He asked me whether he should pay off the debts and in what sequence. That’s a fantastic question.

Here are the partial details of his debts (I’ve concealed the amounts).

-

The primary is a 15 year fixed rate mortgage with a rate of 3%.

-

The secondary is a 5 year ARM with a current rate of 2.5%.

-

The personal loan has a rate of 5%.

Here are my recommendations to him.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Read the rest of this entry »

Share this:

1. “The gross revenues for the financial services industry in 2010 were $1.129 trillion. That year, total US financial assets stood at $50.38 trillion, meaning that the financial services industry as a whole is skimming 2.25% a year out of everyone’s wealth.” This is an excerpt from a post on Wealthcare Capital entitled “Investment Expenses – The Other Millionaire You Make.” How about I help you cut those expenses by half?

1. “The gross revenues for the financial services industry in 2010 were $1.129 trillion. That year, total US financial assets stood at $50.38 trillion, meaning that the financial services industry as a whole is skimming 2.25% a year out of everyone’s wealth.” This is an excerpt from a post on Wealthcare Capital entitled “Investment Expenses – The Other Millionaire You Make.” How about I help you cut those expenses by half?

2. Shocking! Shocking! Your elected representatives want the financial industry to continue ripping you off!

3. Ike Devji wrote a piece “Investment Fraud Red Flag for Physicians.” It is packed full of useful tips. I have one thing to add though, never work with a broker, regardless how clean his or her broker check record. These people are not legally obliged to watch out for your best interest.

4. A very succinct piece in Physicians’ Monday Digest about How Rising Interest Rates Would Affect You.

5. Taxpayers beware, AccountingToday has a piece on tax deductions expiring in 2014.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

The Agony of The Landlord

Posted on: September 5, 2013

A physician client of mine called me the other day and asked my advice as to whether she should evict the tenant currently residing in her condo. This is advice I hate to give. Let me explain.

A physician client of mine called me the other day and asked my advice as to whether she should evict the tenant currently residing in her condo. This is advice I hate to give. Let me explain.The tenant is a single mom with two young children, whose estranged husband just stopped paying child support because he is officially unemployed, but the tenant believes he is getting paid under the table.

My heart goes out to this tenant, I would never want her and her children to become homeless. But my head tells me that if my client lets her stay for free, she would most likely wind up staying for free forever and my client’s rental property would become a toxic asset.

So what should I advise my client?

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

10. P2P Lending: A New Asset Class?

10. P2P Lending: A New Asset Class?

9. A Lesson From a Client: Celebrity Business Gone Bad

8. The High Cost of Fee-Based Financial Advisors

7. How Often Do Market Corrections Happen?

6. Captive Insurance: A Business Owner’s Heaven?

5. How I Helped a Client Save $100k in One Meeting

4. Variable Annuity Fees You Don’t Know You are Paying

2. Be Careful When Buying a Condo as a Rental Property

1. Profit from Harry Dent’s Prediction? Think Again

Also see Top Ten in July.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Request White Paper | Request Discovery Meeting

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

I am not a fan of permanent life insurance. Over the years, I have helped many people extricate themselves from costly life insurance policies. Invariably, they were sweet talked into buying these products without any real need.

I am not a fan of permanent life insurance. Over the years, I have helped many people extricate themselves from costly life insurance policies. Invariably, they were sweet talked into buying these products without any real need.

But recently, I’ve actually had to help a client shop for a permanent life insurance policy. They have a child with a potentially permanent medical condition. Of course we hope and pray that he will outgrow his medical problem, as many kids do, but as parents, they must prepare for the worst.

This is one of the few legitimate reasons for using permanent insurance. Other legitimate reasons include to pay for estate taxes, or to facilitate business succession.

Here is the decision process I employed to help my client, bearing in mind that insurance products are not under the purview of the SEC and are usually chock full of hidden costs.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

What Actually Matters

Posted on: August 28, 2013

This is the title of a newsletter by my peer and friend Russ Thornton. It is fabulously written. I asked his permission to take out a large excerpt:

A recent Onion headline caught my attention. I think I saw it on Google+.

It read . . . Report: Only .00003% Of Things That Happen Actually Matter

The article references a fake Pew Research Center report, and while clearly this is an extreme (and artificial) claim, I think there’s more truth here than fiction.

Especially when it comes to your money and your financial decisions.

Whether it’s the financial media, friends, family, advisors or your psychic, you don’t have to look far for people and organizations eager to tell you what matters with your money. And why.

Interest rates. The price of oil. Trouble in the middle east. Trouble in Washington, DC. Fed tapering. Gold going down. Silver going up.

And the long list goes on.

However, I’d like to suggest a couple of alternatives . . .