Posts Tagged ‘value’

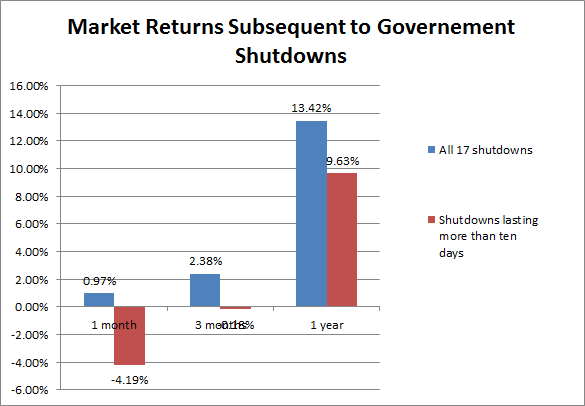

Using the closing price prior to the day of government shutdown as a base line, he found on average, the market rose 0.97% in one month, 2.38% in three months and 13.42% in a year.

If we isolate the 5 most severe shutdowns that lasted more than 10 days, the picture is a bit worse, but not by much. On average the market fell 4.19% in one month, fell .18% in three months and rose 9.63% in a year.

These historical precedents confirm my gut feeling that a government shutdown is really no big deal, as far as the market is concerned.

More worrisome is the upcoming debt ceiling fight. There is no precedent of US default to guide my outlook on this, but the longer the government shutdown lasts, the deeper heels get dug in by both parties and the more likely a default. Nevertheless, I’m still thinking that will also be a storm in a tea cup.

The bottom line is these are issues beyond our control, there is no point worrying about them. If worst comes to worst (ie default,) and the market should drop 20%. That’s actually great because then we can buy shares at a discount!

Share this:

Is a round of golf all the value you get from your financial advisor?

Why do you charge me 1% every year regardless how well you do for me? I would rather not pay you anything for the first 5% return and split anything above and beyond that.

This is a question a prospective client of mine asked me. Let me explain why this fee arrangement is not in the client’s best interest.

Historically, the mean return of the market is 10%, and the standard deviation of return is 15%. This means the market is equally likely to go up 25% in one year and go down 5% in another.

Despite what they want you to believe, financial advisors have very little control over the market.

Share this:

A Simple Investment Principle

Posted on: December 5, 2010

MZ Capital 40/60 model vs S&P 500

Just like two sides of a coin, the capital market is made up of capital demanders (businesses) and capital suppliers (investors). What for businesses are costs of acquiring capital are for investors rewards of supplying it. It is a simple truth that

Costs of Capital = Expected Returns

Looking through this lens, many capital market phenomena can be explained.

Why small stocks tend to have higher returns than large stocks?