Is The Dollar The New Gold?

Posted on: August 2, 2019

“Why are so many countries lending to the US for negative real interest?” Professor Sussman opened the floor for debate at our Oxford macroeconomics class. In totality, foreign countries own $6.2T of US debt. The chart below shows the countries that lend to the US.

In the previous three articles, I wrote about The Gold Standard, The Fiat Money andThe National Saving Shortage respectively. I hope I explained that the trade deficit is recycling of foreign savings for US private investments. And as long as we are paying negative real interest on our national debt, It’s not a problem, but a win to be able to keep borrowing. What I did not explain is why foreign countries would lend to us at negative real interest, and this is exactly what the professor asked in class and what I hope to explain with this article.

Share this:

The National Saving Shortage

Posted on: July 26, 2019

In macroeconomics, there is the balance of payments (BOP) identity …

Imports – Exports = Investments – Savings

This formula is called an identity, not a theory, because it is as true as 1+1=2. The identity basically says if a country imports more than it exports, that is, having a trade deficit, it is because the country does not have enough savings for its investments. (The chart below shows the saving rate of the US in the last few years.) The intuition is this. Foreign countries only have two ways to spend the money they earned from exporting to us, they can either buy our products, or they can lend the money to us. If we have a national saving shortage, we need them to lend us the money, not buy our products. This creates a trade deficit.

Share this:

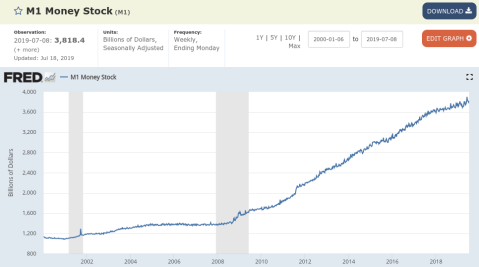

The Fiat Money

Posted on: July 19, 2019

On August 15th, 1971, President Nixon announced that the US would no longer redeem US dollars for gold, thus formally ending the gold standard. During the gold standard, the dollar bill was a certificate of deposit of gold which was redeemable to the bearer on demand. Post-gold standard, the dollar bill is pure paper money, what the academics call fiat money. Read my previous article The Gold Standard.

One immediate consequence was that the government could now issue money at will. And indeed, since 1975, the US has increased the money supply tenfold. As you can see from the chart below, the money printing accelerated in 2009, after the Great Recession. With this level of money printing, we actually need a lot of cheap imports to keep inflation at bay or else there would be too much money chasing too few goods.

The Trade Deficit: Who Is The Winner?

Share this:

The Gold Standard

Posted on: July 12, 2019

|

Share this:

This is actually a response to a client who asked to know what I do regularly that might benefit him. There are many things I could suggest, but I’d like to highlight just three.

Follow academic research

Those of you who have followed me for a while know that I am disdainful of financial news. I liken it to highway noise and I think that listening to it won’t get you anywhere. I am, however, an avid reader of peer-reviewed journals like the Journal of Finance, Review of Financial Studies, etc. These journals contain the best and most rigorous research on the subjects of finance and investment. That’s why I can confidently tell my clients, whatever I do with their money, that I can back up my actions with rigorous peer-reviewed research from the best minds of the world.

Share this:

The Trade War May Be Here To Stay

Posted on: June 3, 2019

The trade deal between the US and China fell through a few weeks ago. Since then, I’ve read at least three versions of what happened, ranging from Trump applying maximum pressure, to Xi reneging, to Xi wanting to do the deal but not being able to get the politburo to go along. Wall Street is hoping Trump and Xi, who will be meeting at the G20 a month from now, can magically salvage the deal. Based on what I’ve read in Chinese media, I am a lot less hopeful. Prior to Trump’s last-minute maximum pressure surprise, I saw the state media was preparing people for a deal; after that, it was preparing people for a long fight.

Bloomberg recently published a study of the economic impact of tariff escalation (see chart below.) As you know, I generally don’t react to the news, but this is looking like a structural change to the world economy that may warrant a reduction in risk exposure. If you are worried, feel free to schedule a time with me to talk about it: http://calendly.com/mzhuang/15min.

Share this:

Shortly after I sent out the last newsletter, my father-in-law told me that his lost money was credited back to his BOA account. This just shows how powerful my newsletter is!

Shortly after I sent out the last newsletter, my father-in-law told me that his lost money was credited back to his BOA account. This just shows how powerful my newsletter is!

OK, I was kidding. Here is what really happened.

After BOA denied his claim twice based on the 60-day excuse, even though the police had already identified the fraudster’s bank account at another bank, my father-in-law filed a claim with CFPB and OCC. (Pop quiz: what are they?) He then wrote a long email to Holly O’Neal, Head of Consumer Client Services of BOA in which he admonished and implored the bank:

Bank of America’s lack of ordinary due diligence in detecting fraud and failing to perform its fiduciary duty resulted in my lost retirement funds. It is disappointing, deplorable and shameful that a global company like Bank of America is dismissive and choosing not to investigate this type of crime, and, instead, closed the fraud claim fast, without offering support or common courtesy to a loyal customer. It is an inhumane treatment of a consumer.

Share this:

Your Bank May Lose All Your Money

Posted on: May 3, 2019

My father-in-law traveled to Taiwan for a few months. When he came back, he went to Bank of America where he maintains a money market account and a checking account to get some money. To his shock, his money market balance which was over $100k before he left was wiped clean, there was not a single dime left.

My father-in-law traveled to Taiwan for a few months. When he came back, he went to Bank of America where he maintains a money market account and a checking account to get some money. To his shock, his money market balance which was over $100k before he left was wiped clean, there was not a single dime left.

It turns out someone had forged his signature in order to create an Electronic Fund Transfer. The forgery is pretty lousy; it does not look like my father-in-law’s signature at all. But that didn’t matter, BOA set up the EFT and proceeded to transfer out all the money, down to the last dime.

He got absolutely no notifications when this was taking place .

You would think that BOA would take responsibility for their oversight. They won’t. They claim that since my father-in-law failed to report the fraudulent transactions within 60 days of their occurrence, they are not responsible for them. Never mind that he was out of the country while his account was being plundered.

Share this:

A few days ago I got a question from a client.

A few days ago I got a question from a client.

Why don’t we move the money to T-Bills to avoid market volatility, and get back to full market exposure only when the market is on an up-trend?

It is all too human to only want to take the upside risk without the downside risk. However, study after study has shown that investors who do that usually end up hurting themselves financially.

Look at the chart. In the fifteen years between 12/31/02 and 12/31/17, missing just 10 of the best return days of the S&P 500 Index would mean that you gave up 66% of the total return during the whole period.

I conjectured that the best return days usually happened at the depth of a bear market when fear and desperation were highest and investors were quitting the market in droves. I asked my assistant Taro to look up historical data to verify that, and here is what he found: the first nine out of the ten best return days in the last fifteen years happened during the Great Recession, just as I had thought!

Share this:

On Dec 17th, 2017, that’s one year and some days ago, BTC (bitcoins) punched through

the $20,000 level, peaking at $20,042.91. Only twenty days earlier BTC reached $10,000 and it was during this 20-day period that I got the most intense client pressures to get their money into BTC and other cryptocurrencies. I am glad I kept them away from it, since as of today, BTC is at $3700. That’s a loss of 81.5% in a year.

BTC is not a stock since it’s not even a real business. Here’s how some stocks that were red-hot a mere few months ago have been faring …

Apple, the perennial darling of the investment world, just lost nearly 40% from its peak after today’s close. That’s a whopping $460 billion loss. The loss itself is larger than the market capitalization of all but four publicly traded companies.

Share this:

- In: Life

- Leave a Comment

1, I got accepted into Oxford University Business School’s Executive MBA program. I will go to Oxford to attend classes starting in January. The program requires me to go to Oxford one week out of every five for a year and a half with a total of sixteen modules.

2, I’ve nearly finished my second book “Entrepreneur Wealth Management Made Easy.” I expect to publish it in the first half of the new year.

Share this:

As of the market close on Monday, December 17th, both the Dow and the S&P 500 have a 14% discount, the Nasdaq has a 18% discount and the small cap Russell 2000 index has a 22% discount.

As of the market close on Monday, December 17th, both the Dow and the S&P 500 have a 14% discount, the Nasdaq has a 18% discount and the small cap Russell 2000 index has a 22% discount.

On the Asian front, the Chinese market has a 27% discount, the Hong Kong market has a 22% discount, and the Japanese market has a 12% discount.

On the European front, the German market has a 21% discount, the UK market has a 14% discount, and the French market has a 15% discount.

According to my wardrobe theory of investment, this is a good time to buy stocks. If you were excited about buying stocks a few months back (when these markets were raising prices to new highs), you should be even more excited now!

(Feel free to share if you find it insightful.)

Schedule a Discovery review with me, or get my white paper for free: The Informed Investor: 5 Key Concepts for Financial Success.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

Investors are extraordinarily good at hurting themselves. They all plan to buy low and sell high, and yet what they all end up doing is buying high and selling low.

Investors are extraordinarily good at hurting themselves. They all plan to buy low and sell high, and yet what they all end up doing is buying high and selling low.

They do that by 1) piling onto the market when it is riding high and bailing when it is dropping low; 2) chasing the immediate past “winner” whether that is gold, emerging market stocks or the S&P 500 only to see the winning streak fizzle. Basically, they are systematically overpaying for assets.

If that sounds like you, well you are not alone. But here is the good news. I am going to give you a simple trick that can help correct your destructive tendency and thereby make you a much better investor.

So are you ready? Drum Roll, please …..

Treat your investment portfolio the same way you would treat your wardrobe.

What are you talking about? Are these two even comparable?

For simplicity’s sake, let say you acquire your entire wardrobe from Neiman Marcus. If Neiman Marcus has an across-the-board 50%-off sale, would you throw up your hands in despair and say,“Darn it, my entire wardrobe just lost half of its value. I better sell it all at the flea market or I will lose everything?”

Share this:

The recent market volatility reminds me of an ancient Greek historian, Thucydides. He wrote “The History of Peloponnesian War,” about the war between the then reigning power Sparta and rising power Athen. He famously wrote: “What made war inevitable was the growth of Athenian power and the fear which this caused in Sparta.”

The recent market volatility reminds me of an ancient Greek historian, Thucydides. He wrote “The History of Peloponnesian War,” about the war between the then reigning power Sparta and rising power Athen. He famously wrote: “What made war inevitable was the growth of Athenian power and the fear which this caused in Sparta.”

Fast forward to two thousand five hundred years later. A Harvard University political scientist, Professor Graham Allison coins the term “The Thucydides Trap” to describe the power dynamic between the reigning power and the rising power. Through an extensive study of historical precedents, he found there are sixteen cases where a major nation’s rise has disrupted a dominant one. Twelve of these ended in wars. For example, the rapid industrialization of Germany rattled Great Britain’s established position at the top of the pecking order, leading to the first World War.

In his book “Destined For War: Can America and China Escape the Thucydides Trap?” Allison argues that this historical metaphor is the best lens through which to observe the US-China relationship.

Share this:

As of yesterday’s closing bell, the Nasdaq Composite is already in correction territory, down more than 12% from its high. However, the other two indices have yet to reach the correction stage, which is marked by a drop of at least 10%: the Dow is down 8.4% while the S&P 500 9.4%.

As of yesterday’s closing bell, the Nasdaq Composite is already in correction territory, down more than 12% from its high. However, the other two indices have yet to reach the correction stage, which is marked by a drop of at least 10%: the Dow is down 8.4% while the S&P 500 9.4%.

I am going to look at the recent market drop from two perspectives: statistical and economical.

Looking through the lens of statistics, a correction is long overdue. Why? Well, the historical odds of a correction are once every two years, those of a bear market once every five years. Yet the last time we had a correction was in 2011, seven years ago. Is it well-overdue?

Looking through the lens of economics, there are two exogenous economic forces that are influencing the market. One is the Trump tax cut, the other is the Trump trade war. These two forces are driving the market in opposite directions.

Share this:

Recently, some of my clients asked me a very good question: “Why is my portfolio not doing as well as the S&P 500 index? Shouldn’t we invest more in US stocks?”

The answer is very simple. US equity is only one component of their portfolio, and it happened to do the best this year. The best component of the portfolio will always do better than the whole portfolio. That does not mean we should not diversify.

In fact, I hear similar questions all the time. Seven years ago, it was “Why didn’t we invest more in emerging markets? There’s no way the US market will do better than emerging markets.” Five years ago, it was “Why shouldn’t we put everything in gold? All of my friends are investing in gold.” In each case, I had to twist their arms to get them to stay invested in US stocks, and now they are thanking me.