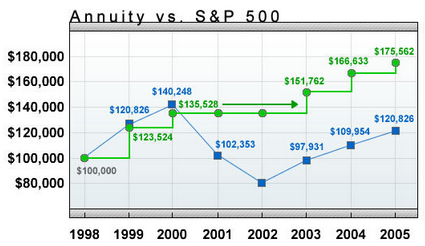

Typical Salesman’s Chart for EIA

Financial author Allan Roth once wrote an article called “Investment Trick – Annuity Style” where he asks a rhetorical question, “If the S&P 500’s total return is 12% in a given year, what do you think your equity index annuity (that is supposed to track the S&P 500) would return”?

- 10%

- 8%

- 5.4%

- 3.4%

Allan Roth goes on to explain why the correct answer is 3.4%. Boy, was he wrong! Read the rest of this entry »

Share this:

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

Recently, we took the money out in favor of a better investment, and boy was she in for a shock! There was a $17k surrender charge and nearly $3.6k in tax withholdings. All the interest she supposedly earned in the annuity went to the surrender charges, and now she has to pay income taxes on that interest!

Here is why a fixed rate annuity is nothing like a savings account.

1. A savings account is FDIC guaranteed, in other words, it has the full faith and credit of the US government behind it. A fixed rate annuity is NOT FDIC guaranteed, it only has the credit of the issuing company behind it. Think AIG! Read the rest of this entry »

Share this:

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Why surrender charges are sunk costs?

Imagine you were sold a $100k variable annuity with a ten year surrender period. The agent who sold you the contract collected a 10% commission, or $10,000. Where do you think this money came from?

Bingo! Your pocket. I hate to break it to you, but insurance companies are not in the charity business and they sure as heck aren’t gonna tell you that 10 of the 100Gs you just handed over to them are going to pay the agent’s commission! If they did that you’d pull your money out and rightly avoid them like the plague in the future.

Share this:

Variable Annuity: Bad Investment!

Posted on: June 5, 2014

Recently I was approached by two prospective clients. The husband is a very successful entrepreneur and they are also very frugal. As the result of that, they have accumulated substantial wealth – north of $5mm.

Recently I was approached by two prospective clients. The husband is a very successful entrepreneur and they are also very frugal. As the result of that, they have accumulated substantial wealth – north of $5mm.

The only problem? all of that money is in about 28 variable annuities they purchased over the years. In examining these variable annuities, I turned up the following problems:

1. Horrible returns

For each variable annuity, I was able to calculate its annualized return.

Out of the 28 variable annuities, only two have annualized returns above 4%. Seven have annualized returns between 3% and 4%. Six have annualized returns between 2% and 3%. The rest (13 of them) have returns less than 2% including a few that have negative returns. The average annualized return? 2.12%. Not enough to beat inflation!

2. Horrible surrender charges

There is this one annuity they purchased from Jackson National Life in 2007 for $200k; today it has grown to a “value” of $245k, but if they should cash it out, they would only get $221k since there is a surrender charge of $24k. After seven years, there is still a surrender charge of 12%! This is just horrible! Read the rest of this entry »

Share this:

On March 19th of this year, the Maryland legislature approved a bill that would raise Maryland’s current state estate tax exemption from its current $1 million leve. The Maryland legislation, which is expected to be signed shortly by Governor Martin O’Malley but as of today it is still awaiting his signature would eventually raise the Maryland state exemption level to the federal estate exemption level.

Currently, assets forming part of a Marylander’s estate upon his or her death in excess of the $1 million threshold would be subject to astate-imposed estate tax this year. Unlike the 2014, federal estate tax exemption amount of $5.34 million. The Maryland legislation provides for the estate tax threshold to continue to rise until it is aligned with the federal estate tax exemption in the year 2019. In 2015, the threshold will be $1.5 million; in 2016, $2 million; in 2017, $3 million; in 2018, 4 million; and finally, in 2019, an amount equal to the federal threshold (which is projected to be $5.9 million in that year once it is adjusted for inflation).

Share this:

I met a couple today (who could become my clients.) The husband is a medical specialist who has been making close to $1mm a year, the wife is a psychologist who was making peanuts. They are both retired now and planning to claim social security incomes.

To maximize their incomes, there is a little-know “File and Suspend” strategy they can use. Here is the gist of it according to Kipinger.

Say you are the higher earner and want to delay until 70. If your wife is 62 or older, she could collect her own benefit — but perhaps she’d get more money with a spousal benefit. One catch: She can’t collect a spousal benefit until you file for your own.

As long as you’re full retirement age, you file for your benefit and your wife applies for a spousal benefit. You ask Social Security to suspend your benefits. Your wife will still receive a spousal benefit, and you can continue to accrue delayed retirement credits until you reapply for benefits, presumably at age 70. Because you’re increasing the value of the survivor benefit, this “file and suspend” maneuver supercharges the survivor benefit for your wife if you die first.

Get informed about wealth building, sign up for The Investment Scientist newsletter

Share this:

Special Need Planning

Posted on: April 7, 2014

Special Need Planning

[A client of mine has two special need kids, so I know how important it is. This is an article I got from a estate planning attorney James Braswell.]

Understanding the pitfalls associated with special needs planning is a must for all who assist families with children, grandchildren or other loved ones (such as parents) with special needs.

Keep in mind these nine tips for Special Needs Planning:

Tip #1: Don’t disinherit your special needs child. Many disabled persons receive Supplemental Security Income (“SSI”), Medicaid or other government benefits that provide basic food, shelter and/or medical care. The loved ones of the special needs beneficiaries may have been advised to disinherit them – beneficiaries who need their help most – to protect the public benefits. But these benefits rarely provide more than basic needs. And this solution (which normally involves leaving the inheritance to another sibling) does not allow loved ones to help their special needs beneficiaries after they themselves become incapacitated or die. The best solution is for loved ones to create a special needs trust to hold the inheritance of a special needs beneficiary. A properly drafted special needs trust will protect public benefits a disabled beneficiary may be receiving, and it will provide for proper care of that individual throughout their lifetime.

Share this:

Investors Good At Hurting Themselves: Investor Returns vs Investment Returns

Posted on: March 18, 2014

Like to hurt yourself?

In 2009, Morningstar did a study comparing mutual fund returns vs investor returns. Here is what they got:

| Fund Category | Fund Return | Investor Return | Investor Lag |

| Large-Cap Blend | -1.4% | -5.7% | -4.3% |

| Large-Cap Growth | -1.7% | -7.7% | -6.0% |

| Large-Cap Value | -1.8% | -2.2% | -0.4% |

| Mid-Cap Blend | 0.4% | -3.0% | -3.4% |

| Small-Cap Blend | -0.5% | -6.9% | -6.4% |

| Europe/Pacific | 3.1% | 0.5% | -2.6% |

| Emerging Markets | 15.6% | 3.8% | -11.8% |

| Financials | -10.5% | -28.6% | -17.9% |

| Health Care | -1.3% | -3.1% | -1.8% |

| Communications | 1.9% | -3.7% | -5.7% |

| Energy | 8.6% | 4.0% | -4.6% |

| REITs | -2.5% | -11.8% | -9.3% |

| Technology | -2.6% | -8.3% | -5.7% |

| Utilities | 5.5% | 2.1% | -3.4% |

| Total and Simple Averages | 1.0% | -3.5% | -4.5% |

Source: Morningstar

We can make a few observations about these data:

Share this:

Disability Planning Gone Wrong

Posted on: March 13, 2014

Many families face hard questions as they decide how to manage the needs of their disabled child after death.

[I got this cautionary tale from a newsletter sent to me by William Fralin, Esq and President of The Estate Planning & Elder Law Firm.,P.C.]

Often, during the parents’ lives a disabled child’s siblings can hold the mantle of responsibility, especially as the parents grow into their golden years. However, this harmonious family dynamic is likely to change after the death of the parents. While many caretaker siblings feel a sense of duty while their parents are alive, and express this sense of duty through the proper care and oversight of the disabled child, this sense of duty often ends when the parents are no longer in the picture. A generation ago, it was common to leave assets to the caretaker sibling in a family in order for that caretaker sibling to see that the needs of the disabled child are met. In fact, this technique was standard practice. However, with so many options available within the realm of modern estate planning it is not necessary, and somewhat risky, to give away assets directly under a moral obligation. One family in California recently experienced the downside of what can occur after the death of a parent.

Share this:

【 Copy from a comment on this news: http://www.msnbc.com/the-last-word/russia-going-lose ]

The scary thing is how easily the American people are conned, again. All it takes is some headlines, no facts, or knowldge of the situation and the people start foaming at the mouth wanting war. Has anyone been paying attention for the last 100 wars and police actions we were conned into, started just like this. Months of intense demonazation of an imagined foe, and then surprise, the evil person does just what was warned about… This classic Iraq and Afghanistan, Iran, Viet Nam, dozens of S.American foes that no one even knew about yet started foaming at the mouth on cue.

Share this:

Are There Rebalance Bonuses?

Posted on: February 24, 2014

Professor Kenneth French

Last month I did a study to understand why equally weighted the S&P 500 index RSP has outperformed value weighted S&P 500 index SPY by almost 3% a year since its inception. My conclusion is that it’s mostly due to Fama French risk factor loading.

However, my research also found after removing the effect of risk factors, RSP has a slight alpha advantage over SPY. I conjecture this alpha advantage is due to the fact that RSP requires annual rebalancing and SPY does not. In other word, this could be the so-called “rebalance bonus.”

To test its robustness, I extended my study to six pair of Fama French “indices.”

Share this:

Despite higher tax rates, S corporations retain advantages over C corporations

Posted on: February 10, 2014

(I got this from Cal Klausner, a CPA friend of mine.)

After recent tax changes, owners of small businesses face a question: Should the business continue to function as an S corporation, or should the entity revoke its election under Subchapter S of the Code?

After recent tax changes, owners of small businesses face a question: Should the business continue to function as an S corporation, or should the entity revoke its election under Subchapter S of the Code?

Despite a number of statutory constraints, conventional wisdom has generally favored an S corporation classification. An S corporation is a pass-through entity whose shareholders are subject to personal income tax based on the income of the corporation. A C corporation, by contrast, is taxed as a separate entity at corporate rates, and its distributions to shareholders are subject to the personal income tax. A small business corporation electing under Subchapter S may have no more than 100 shareholders, and may not have more than one class of stock. There are no similar constraints on C corporations. Nevertheless, an S corporation classification provides business owners a superior degree of flexibility and is therefore generally preferred. Specifically, by having its income flow directly to its shareholders, an S corporation is not subject to the double taxation that a C corporation may be unable to avoid.

Share this:

January Indicator: 2014 Could Be a Year of Opportunity for Wealth Accumulator

Posted on: February 6, 2014

Last year after the market was up about 5% in January, I wrote a newsletter to introduce my clients to the so-called “January Indicator”:

According to research done by Cooper and McConnell, what the market does in January has a strong predictive power for what the market will do for the rest of the year.

Using data since 1940, they found that if the market is up in January, it will rise an additional 14.8% for the rest of the year; if the market is down in January, it will rise only 2.92% for the rest of the year. This gives rise to a spread of almost 12%, a highly statistically significant number.

According to Sam Stovall, chief equity strategist at S&P Capital IQ, the S&P 500 since 1945 has risen 56% of the time following a down January. That is lower than the 84% frequency of February-through-December gains following a higher market in January.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

According to Nobel Laureate Eugene Fama, there are three major risk premiums.

According to Nobel Laureate Eugene Fama, there are three major risk premiums.

1. Equity premium is the additional “wage” one can earn from taking stock market risk over not taking stock market risk.

2. Small cap premium is the additional “wage” one can earn from taking small company risk over taking large company risk.

3. Value premium is the additional “wage” one can earn from taking non-growing company risk over taking growing company risk.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

In the arena of academic finance, the debate over whether a rebalancing “bonus” exists or not has become somewhat of a religion!

In the arena of academic finance, the debate over whether a rebalancing “bonus” exists or not has become somewhat of a religion!

Those who are ardent believers of an efficient market such as Nobel Prize winner Eugene Fama usually believe all returns should be the result of taking risk and that simple actions like rebalancing periodically should not produce additional returns.

Those who believe the market is emotion-driven, such as Nobel Prize winner Robert Shiller, believe in a rebalancing “bonus”. Since the market is either over-priced or under-priced from time to time, rebalancing allows us to take advantage of this market mispricing.

The return differential of RSP vs SPY provides an excellent control experiment to test whether this illustrious rebalancing “bonus” actually exists. SPY and RSP invest in the same 500 largest stocks of the US. SPY being a cap-weighted fund, does not require rebalancing, while RSP being a equally weighted fund requires periodic rebalancing.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter

Share this:

Since its inception on March 9, 2003, RSP has returned 193%. At the same time, SPY has only returned 97%. This is extremely puzzling as both RSP and SPY hold the same S&P 500 stocks.The only difference is that SPY is a cap-weighted fund and RSP is an equally-weighted one. This begs the question, is RSP’s outperformance normal; and more importantly, is it likely to continue?

Since its inception on March 9, 2003, RSP has returned 193%. At the same time, SPY has only returned 97%. This is extremely puzzling as both RSP and SPY hold the same S&P 500 stocks.The only difference is that SPY is a cap-weighted fund and RSP is an equally-weighted one. This begs the question, is RSP’s outperformance normal; and more importantly, is it likely to continue?

To answer the question I asked my intern Nahae Kim to run a regression based on the Nobel Prize winning Fama-French Three Factor Model.

R(x) – rf = alpha + beta1*(Rmkt – rf) + beta2*SML + beta3*HML

Where R(x) is the return of the selected fund, x being either RSP or SPY, alpha is the “skill” of the fund, beta1 is the market risk loading, beta2 is the small cap risk loading and beta3 is the value risk loading.

Here is what I got from the two regressions.

Firm | Youtube | Facebook | Twitter | LinkedIn | Newsletter