Posts Tagged ‘annuity’

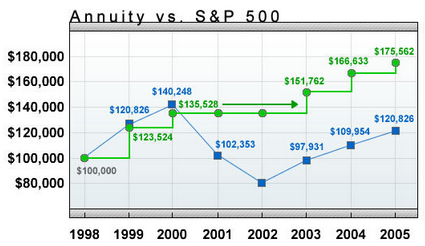

Typical Salesman’s Chart for EIA

Financial author Allan Roth once wrote an article called “Investment Trick – Annuity Style” where he asks a rhetorical question, “If the S&P 500’s total return is 12% in a given year, what do you think your equity index annuity (that is supposed to track the S&P 500) would return”?

- 10%

- 8%

- 5.4%

- 3.4%

Allan Roth goes on to explain why the correct answer is 3.4%. Boy, was he wrong! Read the rest of this entry »

Share this:

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

A client of mine bought a fixed rate annuity a few years ago. She was told by the agent that it’s just like a savings account, only with a higher interest rate of 3%.

Recently, we took the money out in favor of a better investment, and boy was she in for a shock! There was a $17k surrender charge and nearly $3.6k in tax withholdings. All the interest she supposedly earned in the annuity went to the surrender charges, and now she has to pay income taxes on that interest!

Here is why a fixed rate annuity is nothing like a savings account.

1. A savings account is FDIC guaranteed, in other words, it has the full faith and credit of the US government behind it. A fixed rate annuity is NOT FDIC guaranteed, it only has the credit of the issuing company behind it. Think AIG! Read the rest of this entry »

Share this:

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Many people keep their bad annuity investment because it imposes a stiff surrender charge. This is a stereotypical example of sunk cost fallacy, an academic term which describes people throwing good money after bad.

Why surrender charges are sunk costs?

Imagine you were sold a $100k variable annuity with a ten year surrender period. The agent who sold you the contract collected a 10% commission, or $10,000. Where do you think this money came from?

Bingo! Your pocket. I hate to break it to you, but insurance companies are not in the charity business and they sure as heck aren’t gonna tell you that 10 of the 100Gs you just handed over to them are going to pay the agent’s commission! If they did that you’d pull your money out and rightly avoid them like the plague in the future.

Share this:

[Guest Post by Christopher Guest] There are ways a person could use the two year window provided in the Tax Compromise of 2010 to leverage a person’s gifting opportunities, reducing a person’s taxable estate. One strategy that can be used and would not consume any, or only minimally consume, your lifetime gift tax exemption is the Grantor Retained Annuity Trust, or “GRAT.” A GRAT is a form of irrevocable trust that allows the grantor to take a calculated risk to lower the grantor’s taxable estate.

The grantor transfers specific assets or property into the GRAT. The language in the GRAT stipulates that every year the grantor will receive a fixed payment, i.e. an annuity payment, back from the trust over a fixed number of years. A typically time period for a GRAT is 2 to 5 years. At the end of the term, the remainder beneficiaries get whatever is left. For gift tax purposes, the value of the gift is calculated on day one, when the trust is created and funded, but the gift value is discounted, as discussed below.

Share this:

Government Retirees Beware: Your Financial Advisor May Not Be Your Friend

Posted on: January 14, 2012

I have a client (Let’s call him John) who retired 12 years ago from the government. He had a pension, and he had the option of taking out a lump sum of about $800k or drawing a monthly check of more than $4,400 per month until death.

Lost Retirement Money?

John took his options to his financial advisor from Smith Barney (now absorbed into Morgan Stanley Smith Barney.) Guess what the advisor recommended? He recommended that John take out the lump sum and let him manage it instead.

By the time John came to me for a second opinion financial review four years ago, his retirement account had only $265k left. John decided to become my client, and I have been able to restore some of his money, but not all.

Share this:

I recently met an entrepreneur friend of mine. I was pleasantly surprised to learn that he had sold his business and was now looking forward to retirement. He has about $1mm in his 401k plan. As any shameless financial advisor would do, I asked him if he had someone helping him manage his money.

“As a matter of fact, yes!” he answered. “A friend of mine is also a financial advisor, and he helped me create a balanced portfolio.”

He related that “50% of the money will be in safe investment—a (deferred) annuity that has a guaranteed yield of 5%; the other 50% will be in alternative investments for higher performance.”

To say that I was flabbergasted is a serious understatement. With a friend like that, who needs enemies?

Share this:

Invest in a Variable Annuity

Recently, a client of mine brought me the variable annuity he bought a few years ago.

Prominently displayed on the first page are the benefits of the annuity:

Death Benefit: Enhanced Guaranteed Minimum Death Benefit

Living Benefit: Lincoln Lifetime Income Advantage

as well as the fact that the money will earn an fixed annualized rate of 5.75%. Under the bold ACCOUNT FEE subtitle, it states: Account fee is $35 per contract year.

Share this:

Annuity without Risk

Recently, I was approached by a prospective client named John, who has all of his retirement in one annuity.

I have always been intrigued by how annuities and life insurance are sold. Listening to John explain his decision-making process and reading through the annuity contract is like turning on the light bulb in my head.

It turns out that the unique selling point of this product is the “200% Step-Up of the Guarantee Amount (GA).” The way John puts in, if he just keeps the annuity for 10 years, he will get back 200% of what he put in. What is there not to like about that! After all, he gets guaranteed upside with absolutely no downside risk.