Posts Tagged ‘returns’

Typical Salesman’s Chart for EIA

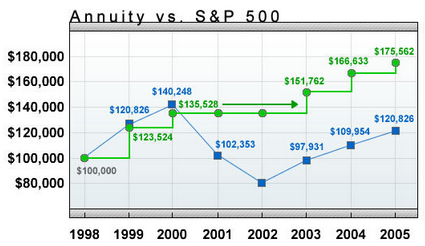

Financial author Allan Roth once wrote an article called “Investment Trick – Annuity Style” where he asks a rhetorical question, “If the S&P 500’s total return is 12% in a given year, what do you think your equity index annuity (that is supposed to track the S&P 500) would return”?

- 10%

- 8%

- 5.4%

- 3.4%

Allan Roth goes on to explain why the correct answer is 3.4%. Boy, was he wrong! Read the rest of this entry »

Share this:

In 1993, the Journal of Financial Economics published “Common risk factors in the returns of stocks and bonds” by Fama and French. They examined bond returns in particular through the lens of various asset return models.

Let’s look at one of those models: the Fama/French three-factor model. The regression statistics of various bond classes are summarized in the table below:

| Bond class | 1-5G | 6-10G | Aaa | Aa | A | Baa | <Baa |

| Alpha | 0.72% | 0.84% | -0.84% | -0.85% | -0.96% | -0.6% | -1.32% |

| Beta | 0.1 | 0.18 | 0.25 | 0.25 | 0.26 | 0.27 | 0.34 |

| S | -0.06 | -0.14 | -0.12 | -0.11 | -0.09 | -0.04 | 0.04 |

| V | 0.07 | 0.08 | 0.14 | 0.15 | 0.16 | 0.2 | 0.23 |